Overview of Underlying Summit Excel Database

Learn how to navigate and interpret the key fields, dynamic data, and specific loan identifiers in the Summit Excel-based BI database for transaction management.

This guide provides an overview of the underlying Excel-based BI database that drives the Summit transaction management system, explaining key columns and how to interpret loan-level data. The goal is to help you accurately track, filter, and manage property acquisitions and securitization variables.

This guide is intended for analysts, data managers, and secondary marketing teams who maintain and verify loan data during asset acquisition and diligence workflows.

Exploring the BI Tape Columns

Loan Identifiers and Diligence

The spreadsheet contains various identifiers used to track and tie reports to diligence vendors.

RMS ID / M3 ID: The primary flat loan numbers.

Servicer ID / Diligence Vendor ID: Use these to tie output reports to specific diligence vendor data.

Acquisition Flow of Funds (FOF)

When reviewing the settlement schedule (FOF), you need to identify the exact purchase price (excluding accrued interest and costs) and the Unpaid Principal Balance (UPB) acquired at that time.

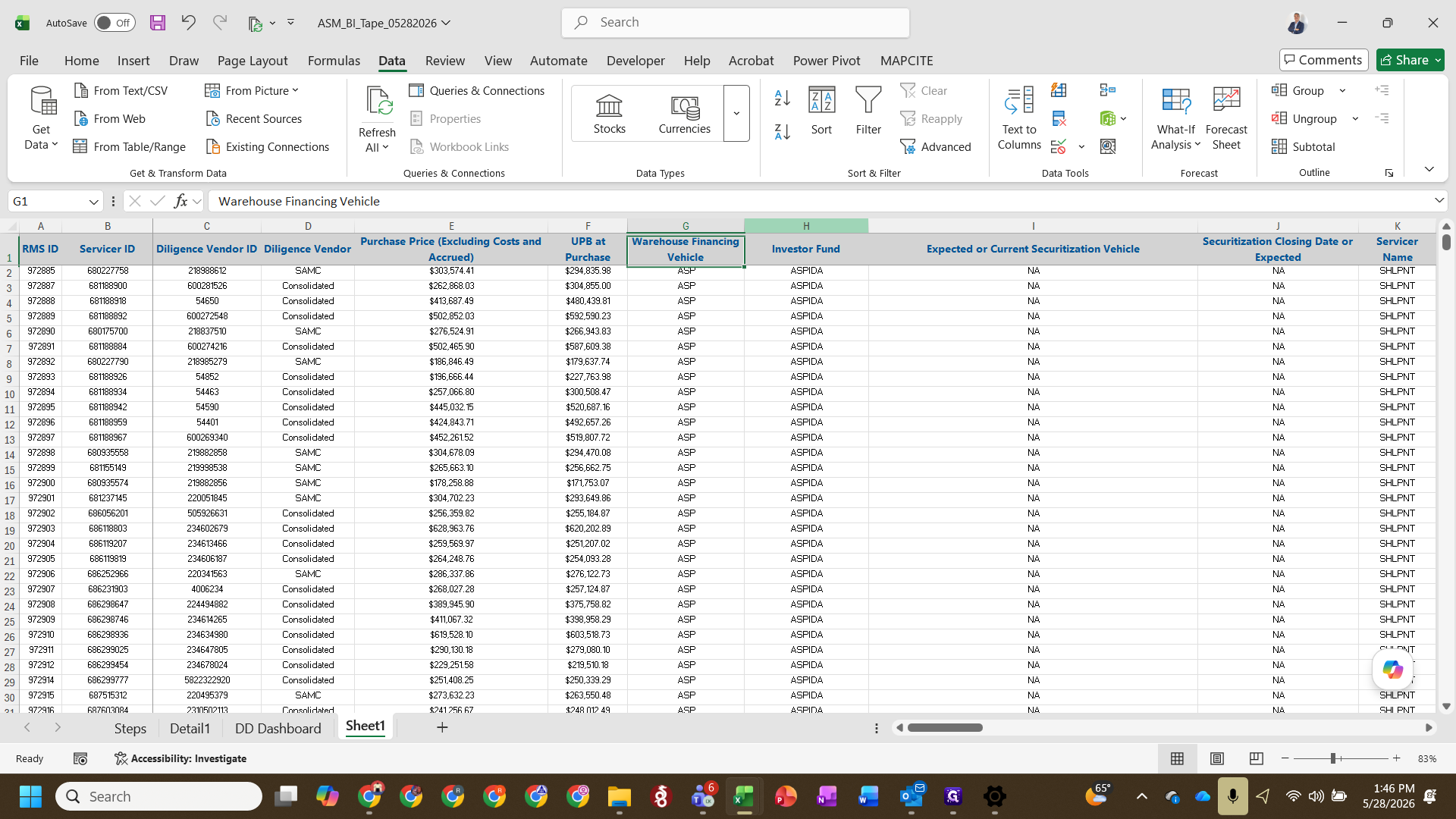

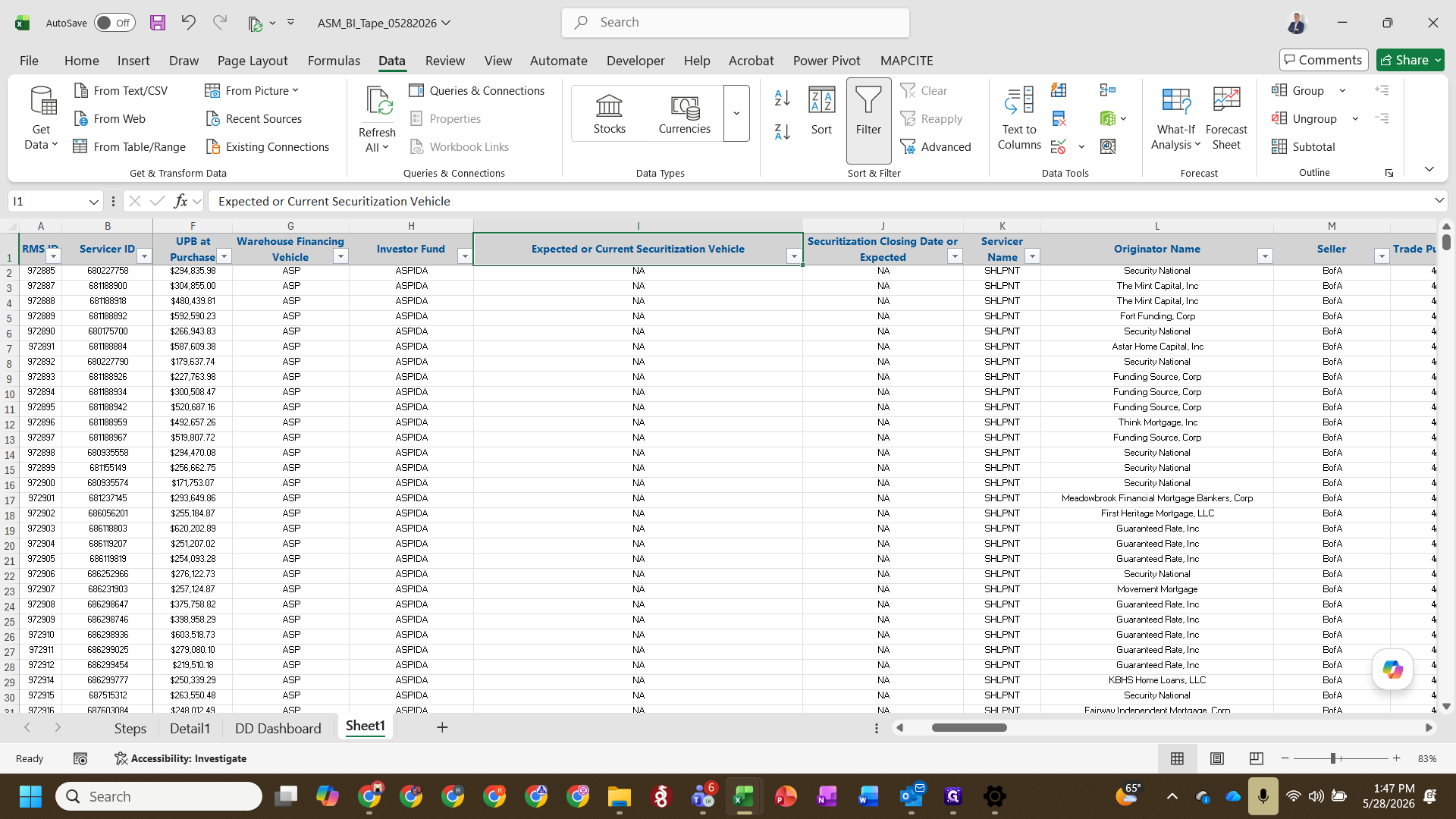

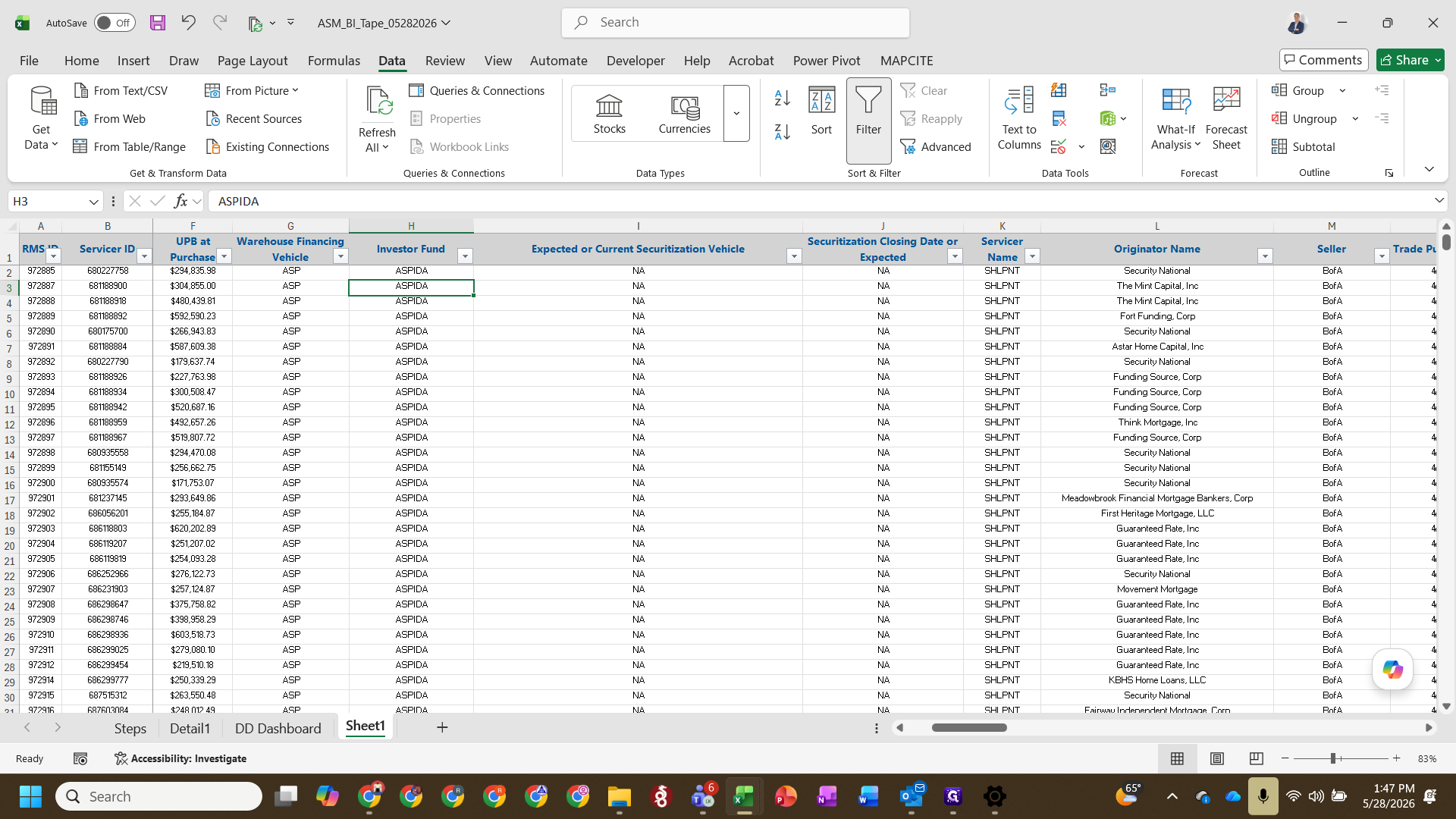

Securitization Vehicles

Identify the investor funds and securitization vehicles backing the deals. For example, ASPIDA provides permanent financing without requiring warehouse financing from banks.

Sellers vs. Originators

Sellers and originators are distinct. A single aggregator (seller) might have a variety of different originators associated with their loans. Ultimately, the correct originator name is found in the Third-Party Review (TPR) data.

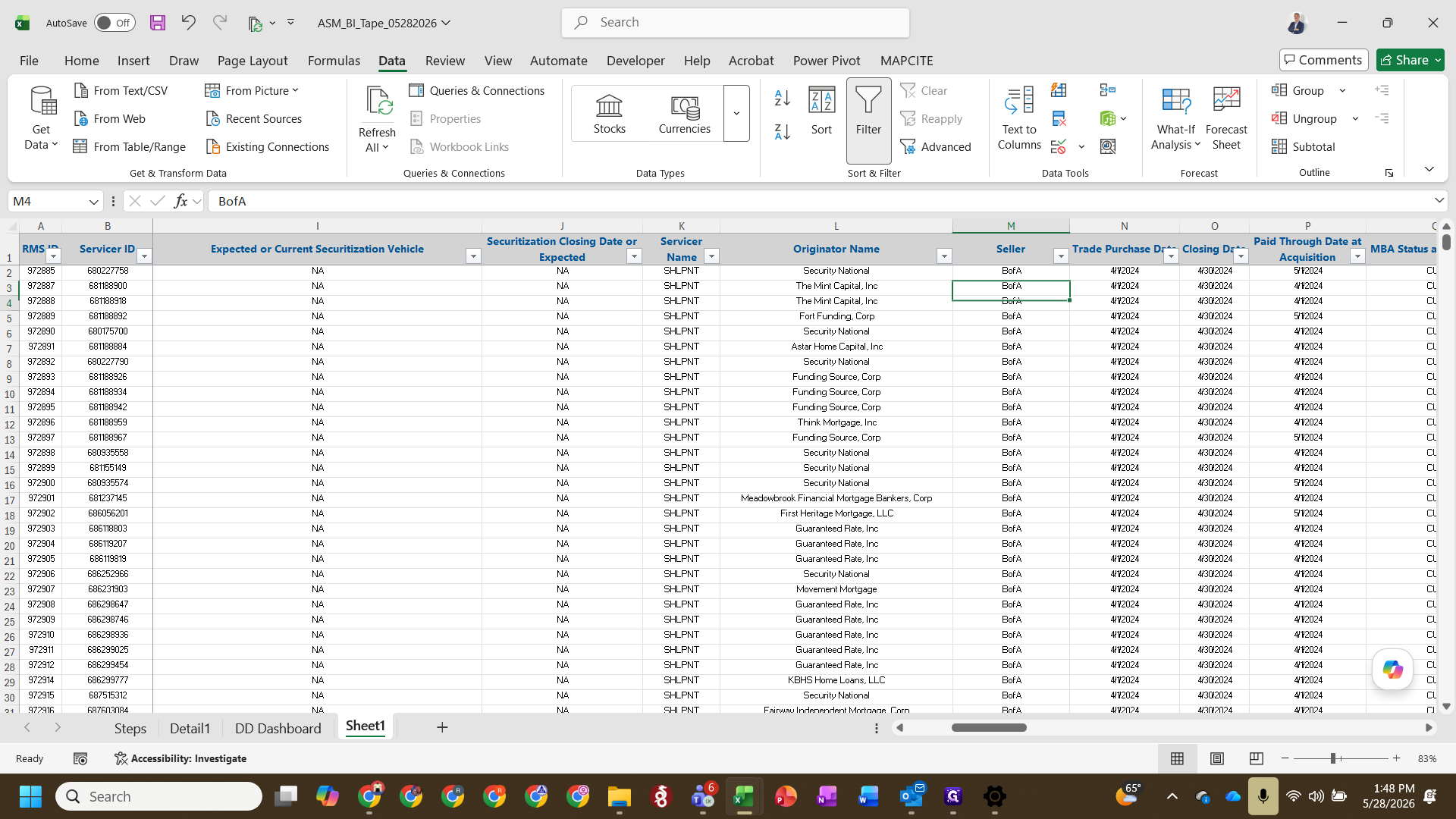

Tracking Trade Dates and Closing Dates

When a trade is locked in, the Trade Date never changes. However, the Target Close Date updates dynamically on a loan-level basis as sellers split trades into multiple fundings or as loans get dropped.

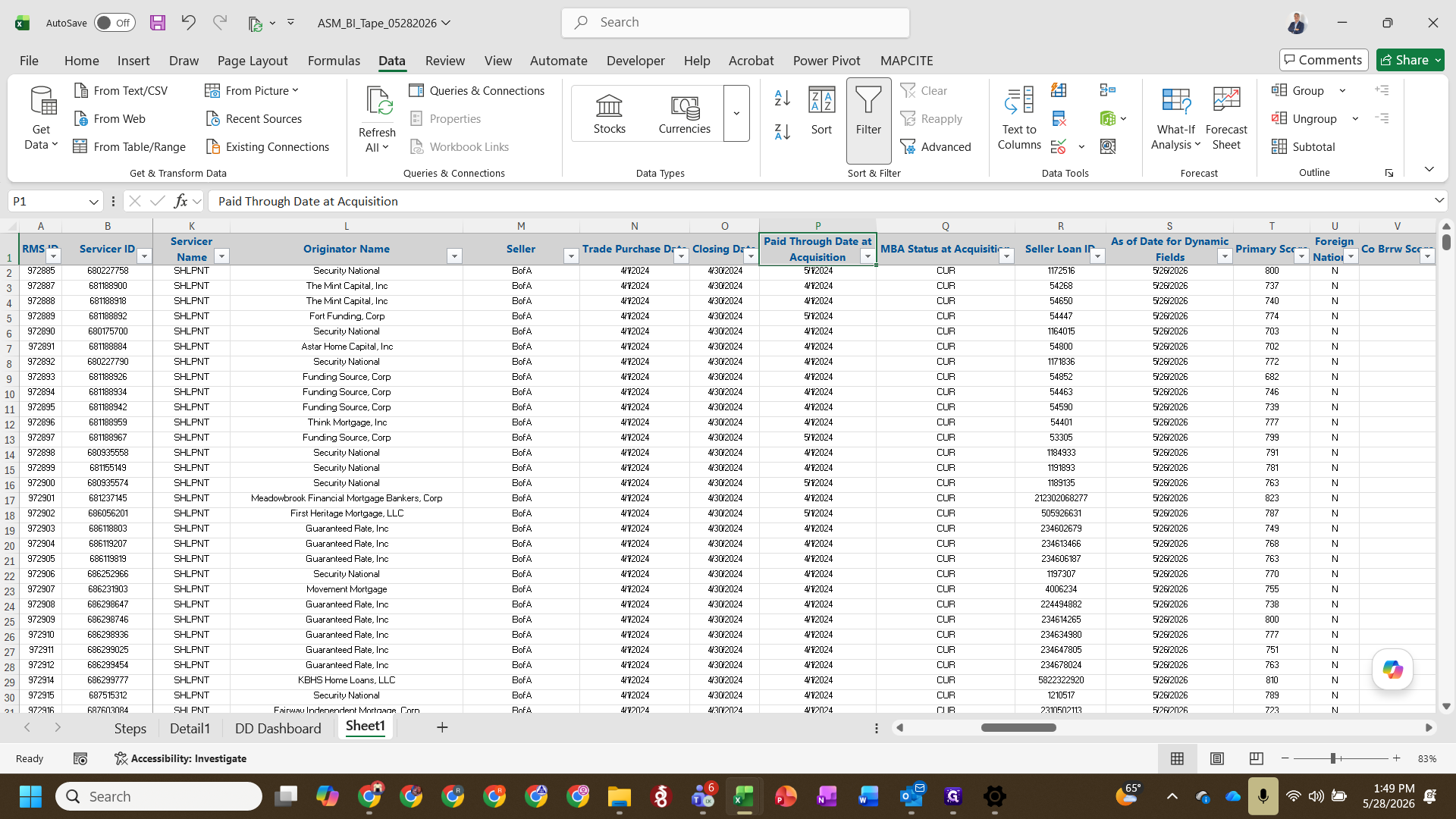

Filtering Unclosed Loans by Paid Through Date

The Paid Through Date at Acquisition reflects the Interest Pay Through Date (IPD) seen on the settlement schedule. You can use this column to quickly identify loans that have not yet had a settlement.

Standard Non-QM Data Fields

Everything to the right of the seller loan data contains standard fields required to track and price Non-Qualified Mortgages (NQMs).

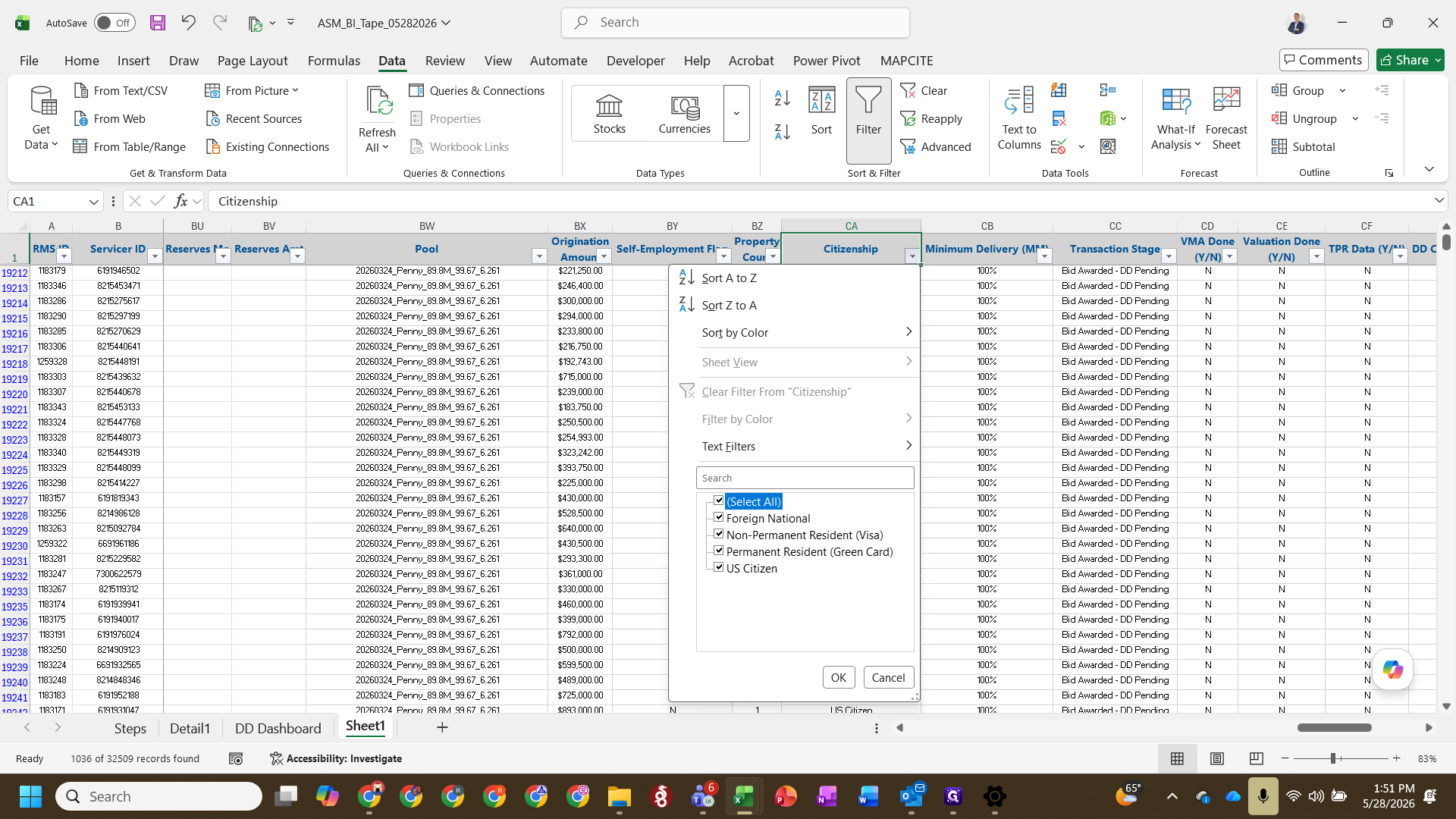

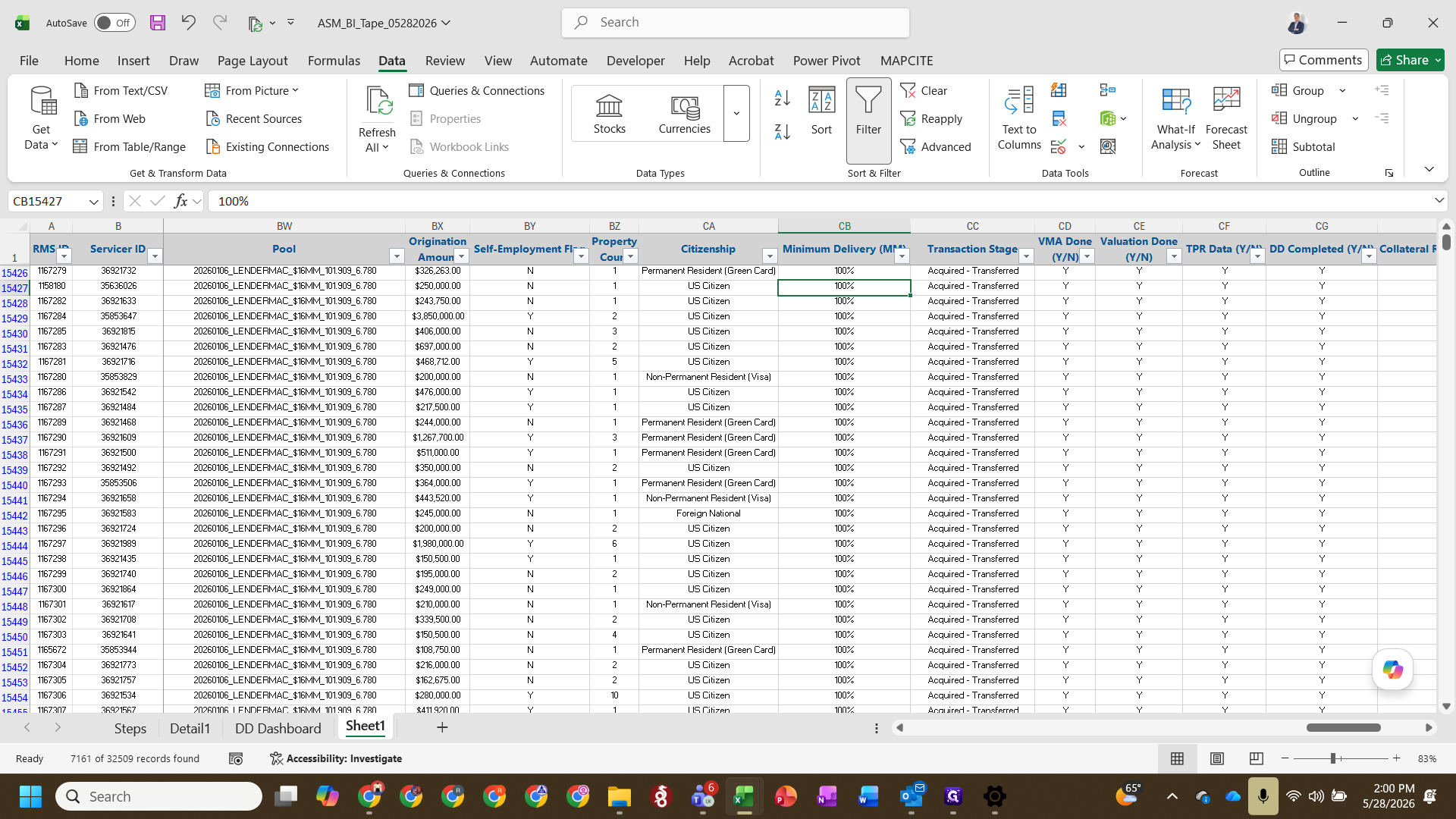

Citizenship and Foreign Nationals

Citizenship Status | Description |

|---|---|

US Citizen | Standard US citizenship status. |

Permanent Resident | Green card holders. |

Non-Permanent Resident | Individuals residing in the US with a visa. |

Foreign National | Triggers the "Yes" flag in the Foreign National column. |

Loan-to-Value (LTV) vs. Combined LTV (CLTV)

Compare LTV and CLTV to identify junior liens.

If CLTV matches LTV, there are no junior liens.

If CLTV is higher than LTV, the property likely has another lien (junior lien).

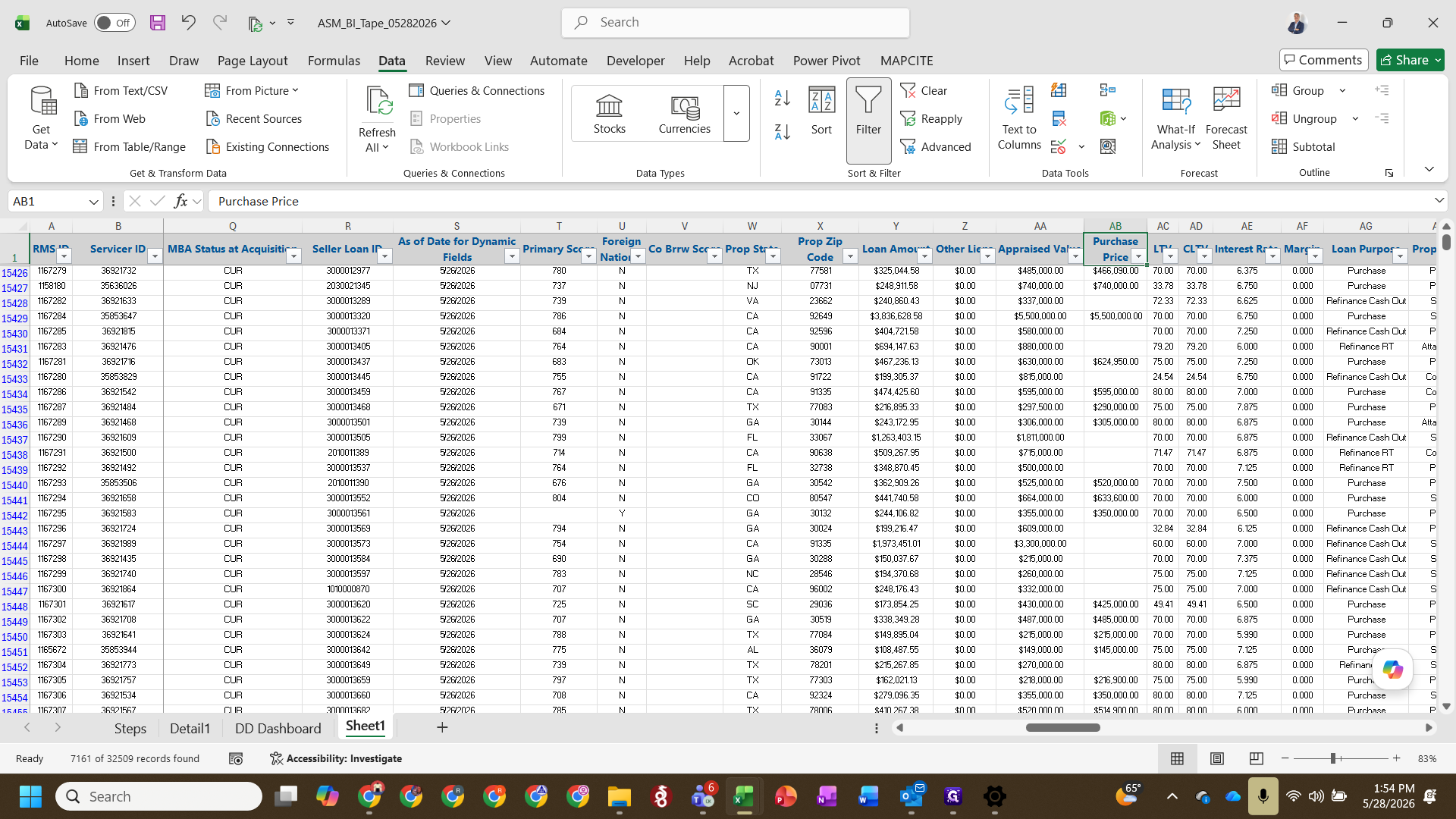

Purchase Price Discrepancies

Loans marked with a "Purchase" loan purpose should always have an associated purchase price. If they don't, this indicates a data discrepancy.

Property and Occupancy Types

Differentiate property occupancies carefully. Investment properties and secondary homes are both considered non-owner occupied, but they carry different risk profiles and must be bifurcated for NQM pricing.

Ratios and Debt Service

Different ratios apply depending on the loan and property type:

Ratio Type | Description |

|---|---|

Front-End DTI (Top Ratio) | Evaluates the borrower's debt-to-income ratio using only the specific mortgage debt. |

Back-End DTI (Bottom Ratio) | Evaluates the borrower's debt-to-income ratio including all other existing debt service. |

DSCR (Debt Service Coverage Ratio) | Evaluates property cash flow rather than personal income; used primarily for investment properties. |

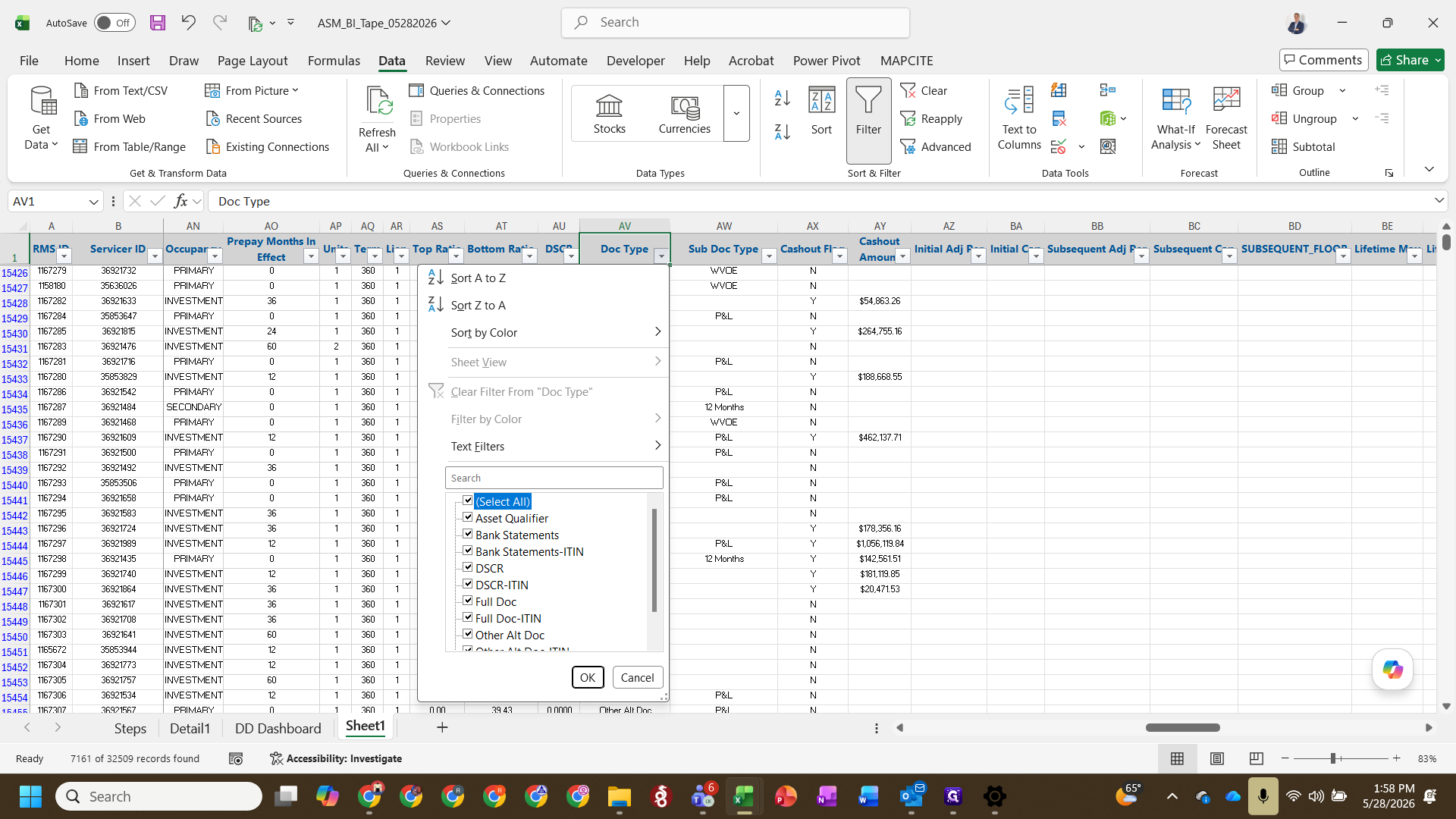

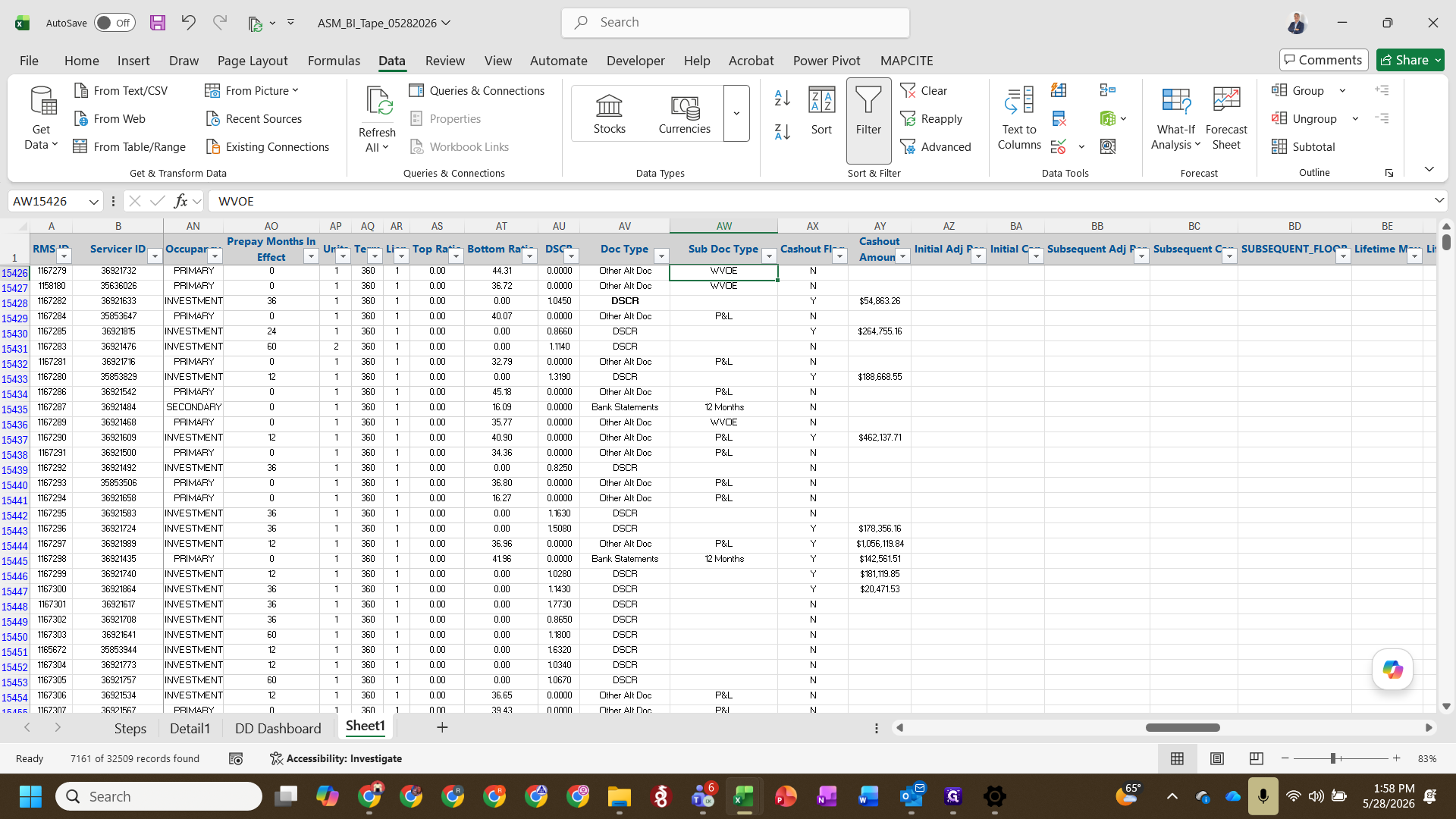

Alternative Document Types

Document Category | Examples |

|---|---|

Bank Statements | 12-month or 24-month bank statements used for income verification. |

Alternative Docs | WVOE (Written Verification of Employment), retirement income, or tax returns. |

Business P&L | Business profit and loss statements or business tax returns for self-employed borrowers. |

Pool Deliveries and Minimum Delivery Percentages

Some bids might add $200 million worth of loans to a pool but only require $100 million to be delivered.

Q: Why is there no purchase price for a loan marked with a "purchase" purpose?

A: This is a data discrepancy that occasionally occurs on the tape. These should be flagged to the team using "See Something, Say Something" (SSSS) emails.

Q: Why are the ASPIDA cells marked as N/A for warehouse financing?

A: ASPIDA relies on their own insurance partners to fund deals without needing temporary warehouse financing from a bank or asset-backed securitizations.

Q: Does a trade date change after a trade is locked in?

A: No, the trade date never changes. However, the target close date will often be updated dynamically on a loan-level basis.

Q: How do you identify if a loan has a junior lien?

A: Compare the Loan-to-Value (LTV) and Combined Loan-to-Value (CLTV). If the CLTV is higher than the LTV, there is likely a junior lien attached to the property.

Term | Definition |

|---|---|

NQM (Non-Qualified Mortgage) | A type of home loan that does not comply with the standard borrowing guidelines set by regulatory agencies. |

UPB (Unpaid Principal Balance) | The portion of a loan's principal that has not yet been paid back to the lender. |

FOF (Flow of Funds) | A settlement schedule detailing the exact purchase price and amounts transferred during an acquisition. |

IPD (Interest Pay Through Date) | The date through which interest has been successfully paid on a specific loan. |

DTI (Debt-to-Income) | A personal finance metric that compares an individual's monthly debt payments to their monthly gross income. |

DSCR (Debt Service Coverage Ratio) | A metric used in investment property lending that measures a property's cash flow against its debt obligations. |

TPR (Third-Party Review) | An independent evaluation process used during due diligence to verify originator and loan data. |

ARM (Adjustable-Rate Mortgage) | A home loan with an interest rate that can change periodically over the lifetime of the loan based on specific indices. |

LTV (Loan-to-Value) | An assessment of lending risk that compares the initial loan amount to the appraised value of the property. |

CLTV (Combined Loan-to-Value) | The ratio of all loans on a property, including any junior liens, compared to its appraised value. |