Read summarized version with

The first time I really understood the accounts payable problem, I was sitting in a conference room at a multi-unit restaurant operator.

The AP Manager I’ll call Linda had been processing invoices the same way for years. Two monitors. An ERP. A Rolodex of vendor quirks living entirely in her head. When I asked how she’d train a replacement, she laughed it off — every attempt had ended with the new hire quitting.

That same pattern shows up again and again in AP. I’ve talked to leads who’ve built dozens of separate guides for processing invoices, one for every edge case, vendor quirk, and coding rule, just so the company could keep paying its bills if they ever stepped away.

That’s the accounts payable problem in a nutshell. AP looks routine from the outside, but most of the real work runs on tribal knowledge that lives in one or two people’s heads. When that knowledge walks out the door, vendors don’t get paid, discounts get missed, and audits go sideways.

I’m Yuval, CEO of Glitter AI. We help finance teams document their AP process so it survives turnover. This guide is what I’ve learned from working with AP teams about what an actual accounts payable SOP looks like, and how to write one without losing your mind.

Teach your co-workers or customers how to get stuff done – in seconds.

What Is an Accounts Payable SOP?

An accounts payable SOP is a documented, step-by-step procedure for how your company handles money owed to vendors, from the moment an invoice arrives to the moment payment clears. It covers vendor onboarding, invoice intake, matching, approval, GL coding, payment, and the controls keeping all of that from going wrong.

For the broader context on standard operating procedures, my deep dive on documenting the accounting department covers the full finance department picture, and our glossary entry on standard operating procedures covers the definitional background.

A good AP SOP answers four questions at every step:

- Who owns it? (the role, not the person)

- What system do they use? (and which specific clicks)

- What controls exist? (segregation of duties, approval thresholds)

- What can go wrong? (and how to handle it)

Most AP “documentation” I run into fails on at least three of those four. It tells you what to do but not who does it. Or it lists controls without showing the screens where those controls are actually applied.

Why Most AP Teams Don’t Have Real SOPs

Before getting into the process, it’s worth understanding why this gap keeps showing up.

Accounts payable is one of the most repetitive functions in finance, and it sits inside a wider set of best practices for an accounting department SOP that most teams never formalize. Whoever owns it has usually been doing it the same way for years. There’s no immediate pain. Invoices get paid, vendors aren’t calling, so writing it down feels like overhead. Then someone goes on vacation, retires, or quits, and suddenly nobody knows how to apply that one weird credit memo from that one vendor, because the invoice management process was never written down.

The other reason is that AP work is screen-heavy, which is why solid QuickBooks workflow documentation is so rare. Showing someone how to enter an invoice in QuickBooks or Sage is genuinely hard to do in writing. By the time you’ve described every menu, every checkbox, and every keyboard shortcut, you have a 30-page document nobody will read.

This is the exact problem we built Glitter AI to solve. You record yourself doing the task once, clicking through QuickBooks or Sage in real time, and you get a step-by-step guide with screenshots, edits, and shareable links. Record once, train forever.

Glitter AI records your screen and turns it into a step-by-step SOP automatically

The Full AP Cycle: Step by Step

Here’s the complete accounts payable workflow your SOP needs to cover. I’ll walk each stage with the owner, the controls, the common failure modes, and what to actually document.

1. Vendor Setup and W-9 Collection

Who owns it: AP Specialist or AP Clerk, with Controller approval for new vendors above a threshold.

Vendor setup is where AP fraud usually starts, so a disciplined vendor onboarding process matters more than it looks. A fake vendor record is worth more than a fake invoice, because once the vendor is in your system, ongoing vendor management is the only thing keeping every payment to it legitimate.

What to document in your SOP:

- The intake form for new vendors (legal name, DBA, remit-to address, payment terms, tax ID)

- W-9 collection process and where the W-9 lives

- Verification steps (call the vendor at a known number, confirm bank details out-of-band)

- Who approves new vendors and at what dollar threshold

- How to flag 1099-eligible vendors at setup (this saves you in January)

Common errors: Skipping the call-back verification. Missing W-9s for 1099 vendors. Duplicate vendor records that allow duplicate payments.

Key control: Segregation of duties. The person who sets up vendors should never be the person who approves payments to them.

2. Purchase Order Generation

Who owns it: Department requestor or buyer, approved by department head.

Not every company uses POs, and that’s fine for low-dollar recurring expenses. But for inventory, capital purchases, and anything above your PO threshold, the PO is the foundation of three-way matching.

Document in your SOP:

- When a PO is required (dollar threshold, category)

- Who can issue POs and approval routing

- How POs are numbered and tracked

- The approval workflow before the PO is sent to the vendor

Common errors: Retroactive POs created after the invoice arrives. POs with vague descriptions that make matching impossible.

3. Invoice Receipt and Intake

Who owns it: AP Clerk.

Invoices arrive through email, mail, vendor portals, or, in some shops I’ve visited, physical fax machines that nobody admits exist. Your SOP needs to cover all of them.

Document:

- The single intake inbox (

ap@yourcompany.comis standard) - How to log the invoice (date received, vendor, amount, invoice number)

- How to scan and store paper invoices

- Naming conventions for invoice files

Common errors: Invoices going to individual employees’ inboxes and getting lost. Duplicate invoice numbers from the same vendor missed because intake isn’t centralized.

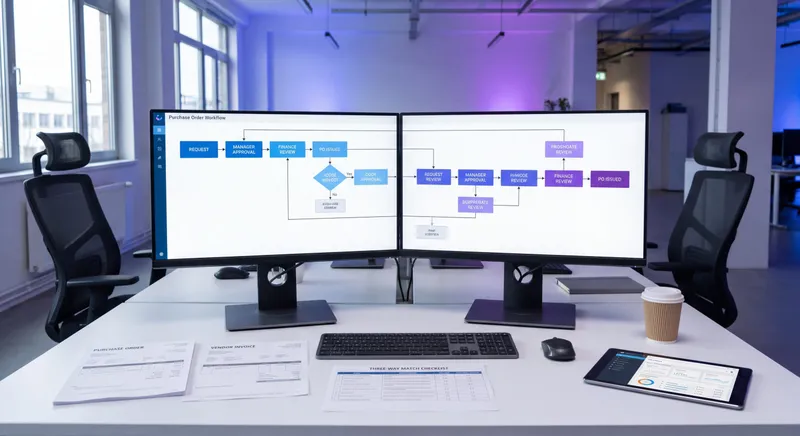

4. Three-Way Matching

Who owns it: AP Specialist.

Three-way matching lines up the invoice against the purchase order and the receiving document, and it sits at the heart of the broader accounts payable workflow. All three should agree on quantity, price, and item. If they don’t, the invoice goes into exception handling.

Your SOP should walk through:

- The exact screens in your ERP where matching happens (this is where Glitter shines, record it once)

- Tolerance thresholds (how much variance triggers an exception)

- What to do when the receiving document is missing

- How to handle partial shipments

Common errors: Tolerances set too loose, so overcharges sail through. Receiving never entered in the system, so matching fails for legitimate invoices. Manual overrides with no paper trail.

Key control: Tolerance thresholds approved by the Controller, not the AP Specialist.

5. Invoice Approval Workflow

Who owns it: Department head or budget owner. AP routes; they approve.

For non-PO invoices, you need an approval workflow tied to dollar thresholds and to department.

Document:

- Approval matrix (who approves what, at what dollar level)

- How invoices get routed (email, ERP workflow, paper folder)

- SLA for approval (how long approvers have before AP escalates)

- Escalation path when approvers are out

Common errors: Approval bottlenecks at one person who’s always traveling. No escalation path, so invoices sit for weeks. Approvers rubber-stamping without actually checking.

6. GL Coding

Who owns it: AP Specialist, with Controller review.

Every invoice gets coded to a general ledger account. Bad coding doesn’t stop payment, but it wrecks your financial reporting and gives auditors heartburn.

Document:

- Your chart of accounts (or a simplified AP-facing version)

- Coding rules for common vendors (e.g., “AT&T always goes to 6420 - Telecom”)

- How to handle invoices that span multiple GL accounts (allocations)

- How to code prepaids, fixed assets, and capitalized expenses correctly

Common errors: Defaulting everything to “Office Supplies” because the coder doesn’t know the right account. Skipping prepaid treatment for annual invoices.

7. Payment Scheduling

Who owns it: AP Manager or Controller.

When you pay matters as much as how much. Pay too early and you give up working capital. Pay too late and you damage vendor relationships and miss early-pay discounts.

Document:

- Payment terms by vendor (Net 30 is not the only term in your system, I promise)

- How discount terms (2/10 Net 30) are flagged and captured

- Cash flow review before each payment run

- Hold conditions (vendor disputes, missing W-9, credit memos pending)

8. Payment Run: Check, ACH, Wire

Who owns it: AP Manager prepares; Controller or CFO approves and releases.

The payment run is the highest-control moment in the AP cycle. This is where your segregation of duties either holds up or it doesn’t.

Document:

- The payment selection process (which invoices, how they’re approved into the run)

- Check signing rules and dual signature thresholds

- ACH file generation, banking portal upload, and approval

- Wire transfer call-back verification (always, no exceptions, for any new wire instructions)

- Positive pay setup with your bank

Common errors: The same person who creates the payment file also releases it. Wire fraud from spoofed vendor emails. That last one happens constantly and costs SMBs millions.

Key control: Two people on any wire. Always.

9. Exceptions and Disputes

Who owns it: AP Specialist, with escalation to AP Manager.

Document the exception types you actually see (price variance, quantity variance, missing PO, duplicate invoice, vendor dispute), and lay out the resolution path for each.

Your SOP should include:

- Exception log (where it lives, who reviews it weekly)

- Dispute resolution timeline

- When to involve purchasing vs. when AP handles it

- Credit memo handling and application

10. Month-End Accruals

Who owns it: Controller or Senior Accountant, with AP support.

At month-end you need to accrue for goods or services received but not yet invoiced. This is the seam where AP and the close process meet.

Document:

- The cutoff date and time for invoice entry

- How to identify unaccrued liabilities (open POs received but not invoiced)

- The accrual journal entry template

- Reversal in the following period

11. 1099 Preparation

Who owns it: AP Manager, with Controller review.

If you flagged 1099 vendors back at setup (step 1), January is mostly a verification exercise. If you didn’t, January is hell.

Document:

- The 1099-eligible vendor flag and how to set it

- Annual W-9 refresh process

- Reconciliation between AP payments and 1099 totals

- Filing process and deadlines (1099-NEC, 1099-MISC)

Teach your co-workers or customers how to get stuff done – in seconds.

Sample Step-by-Step: Processing an Invoice in QuickBooks

Here’s what a real AP SOP step looks like for invoice entry. This is the level of detail your documentation needs.

Process: Enter a vendor invoice in QuickBooks Online

- Open QuickBooks Online and navigate to + New in the top left

- Under “Vendors,” select Bill

- In the Vendor dropdown, search for the vendor (verify the legal name matches the invoice)

- Enter the Bill date (date on the invoice, not today’s date)

- Enter the Due date based on payment terms

- Enter the Bill no. exactly as shown on the invoice (this prevents duplicates)

- Under Category details, select the GL account per your coding rules

- Enter the description and amount

- Attach the invoice PDF using the paperclip icon

- Click Save and close

For Sage 100 or other ERPs, the steps differ but the principle holds: every click, every field, every validation rule needs to live in your SOP. This is the kind of process where my QuickBooks training guide and a parallel Sage Paperless walkthrough work well as references for your team.

AP SOP Template Structure

Every AP SOP in your library should follow the same shape. Consistency makes it easier to find information, and easier to train new hires.

Header

- SOP title

- Owner (role, not person)

- Last updated date

- Next review date

- Approver

Purpose

One paragraph: why this SOP exists and what it controls.

Scope

What’s covered, what’s not. Which entities, departments, or vendor types apply.

Roles and Responsibilities

Who does what. Use roles, not names.

Procedure

The actual step-by-step. Numbered. With screenshots if it’s a software-based task.

Controls

What controls are embedded in the process. Approval thresholds, segregation of duties, system controls.

Exceptions

Common edge cases and how to handle them.

References

Related SOPs, policies, system documentation.

Revision History

Date, change, who changed it.

Segregation of Duties: The Non-Negotiables

Even at small companies, you need basic segregation in AP. The minimum acceptable split looks like this:

- Vendor setup and payment approval must be different people

- Invoice entry and payment release must be different people

- Bank reconciliation should be done by someone outside AP entirely

If you’re genuinely a one-person AP shop, the Controller or owner becomes the second pair of eyes. Document who that is and what they review. “We’re too small for SOX” is not a defense an auditor will accept.

For a fuller picture of how AP fits into the wider finance function, my walkthrough of the broader accounting playbook covers month-end close, reconciliations, and the rest of the controls landscape.

The Tribal Knowledge Problem (And How to Actually Fix It)

I want to come back to the AP-veteran story, because it’s the one I see most often.

A long-tenured AP person knows the job cold. They know which vendors need special handling, which invoices to hold for the GM’s review, which coupons apply to which GL account. Years of that knowledge lives in their head. The company has no AP SOP because, in their minds, that person is the SOP.

The day they decide to retire, the CFO calls in a panic. A couple of months to extract everything they know before they walk out the door. A couple of months to write down years of muscle memory.

That’s the wrong way to do this. The right way is to document continuously, not under duress. And the documentation should be created by the person doing the work, not by some consultant trying to interview them.

That’s what we built Glitter AI for. The outgoing AP person records themselves doing each task (entering an invoice in Sage, processing a vendor credit, reconciling a statement) and Glitter generates the step-by-step guide with screenshots automatically. A handful of recordings in the final weeks can shrink replacement ramp from months to a few weeks.

To see what that workflow actually looks like, the Glitter AI SOP generator is built for exactly this. Record once, train forever.

How to Roll Out an AP SOP Project

If your AP function has zero documented procedures today, don’t try to write everything at once. Here’s the order I’d recommend:

- Start with the highest-risk processes: vendor setup, payment runs, wire transfers

- Document the most-repeated processes next: invoice entry, three-way matching, approval routing

- Tackle the edge cases last: disputes, exceptions, year-end 1099 prep

- Schedule quarterly reviews: every SOP gets re-read and updated, or it rots

Don’t try to make every SOP perfect on day one. A flawed SOP that exists beats a perfect one that doesn’t.

Glitter AI captures your screen and turns it into a polished SOP your team can actually follow

What Good AP SOPs Look Like in Practice

The teams I’ve worked with who get this right share a few habits:

- Their SOPs are short. Two to four pages each. One process per document.

- Their SOPs have screenshots. Every system step shows the actual screen.

- Their SOPs are findable. A central library, not scattered across someone’s OneNote.

- Their SOPs are reviewed. Quarterly, with the date stamped on the document.

- Their SOPs are written by the people who do the work. Not by an outside consultant.

That last point is the one most companies miss. The person doing the job is the only person who really knows what the job involves. Your SOP project should let them document on their own, not pull them into a conference room for two-hour interviews.

Frequently Asked Questions

What is an accounts payable SOP?

An accounts payable SOP is a documented procedure that defines how your company processes invoices, approves payments, and pays vendors. It covers the full AP cycle from vendor setup through payment and includes the controls, owners, and exceptions for each step.

What should an AP SOP include?

A complete AP SOP should cover vendor setup and W-9 collection, PO generation, invoice intake, three-way matching, approval routing, GL coding, payment scheduling, payment runs, exception handling, month-end accruals, and 1099 preparation. Each section should specify the owner, the system steps, the controls, and common errors.

Who is responsible for writing the accounts payable SOP?

The AP Manager typically owns the SOP, with input from the Controller and the AP Specialists who do the daily work. The best AP SOPs are written by the people performing the tasks, not by outside consultants, because they know the real edge cases and system quirks.

What is three-way matching in AP?

Three-way matching compares an invoice to the purchase order and the receiving document to confirm that quantity, price, and item all agree before payment. It is one of the most important AP controls and prevents overpayment, duplicate payment, and payment for goods never received.

What are the most important AP controls to document?

The most important controls are segregation of duties between vendor setup and payment approval, dual approval on wire transfers, three-way matching tolerances, approval thresholds tied to dollar amounts, and call-back verification for any new banking instructions from vendors.

How do I document AP procedures in QuickBooks or Sage?

The most effective way is to record your screen while performing the task and let an SOP tool like Glitter AI generate the step-by-step guide with screenshots. Writing software steps by hand is slow and produces documents people will not read. Recording captures every click in real time.

What is segregation of duties in accounts payable?

Segregation of duties means splitting AP responsibilities so no single person can both initiate and approve a payment. At minimum, vendor setup, invoice entry, payment approval, and bank reconciliation should be performed by different people, or supplemented with a second reviewer in small teams.

How long should an accounts payable SOP be?

Each individual AP SOP should be two to four pages and cover one process. A 30-page master document nobody reads is worse than ten focused two-page SOPs your team actually uses. Keep one process per document and link related SOPs together.

How do I handle 1099 preparation in my AP SOP?

Flag 1099-eligible vendors at the time of vendor setup, collect a W-9 before the first payment, and reconcile annual AP payments to 1099 totals each January. If you wait until year-end to identify 1099 vendors, you will spend weeks chasing W-9s and risk filing penalties.

What is the best way to prevent AP fraud?

The most effective controls are vendor setup verification with call-back to a known number, segregation of duties between vendor setup and payment approval, dual approval on wires, positive pay with your bank, and out-of-band verification for any change to vendor banking instructions. Most AP fraud starts with a fake or compromised vendor record.