Read summarized version with

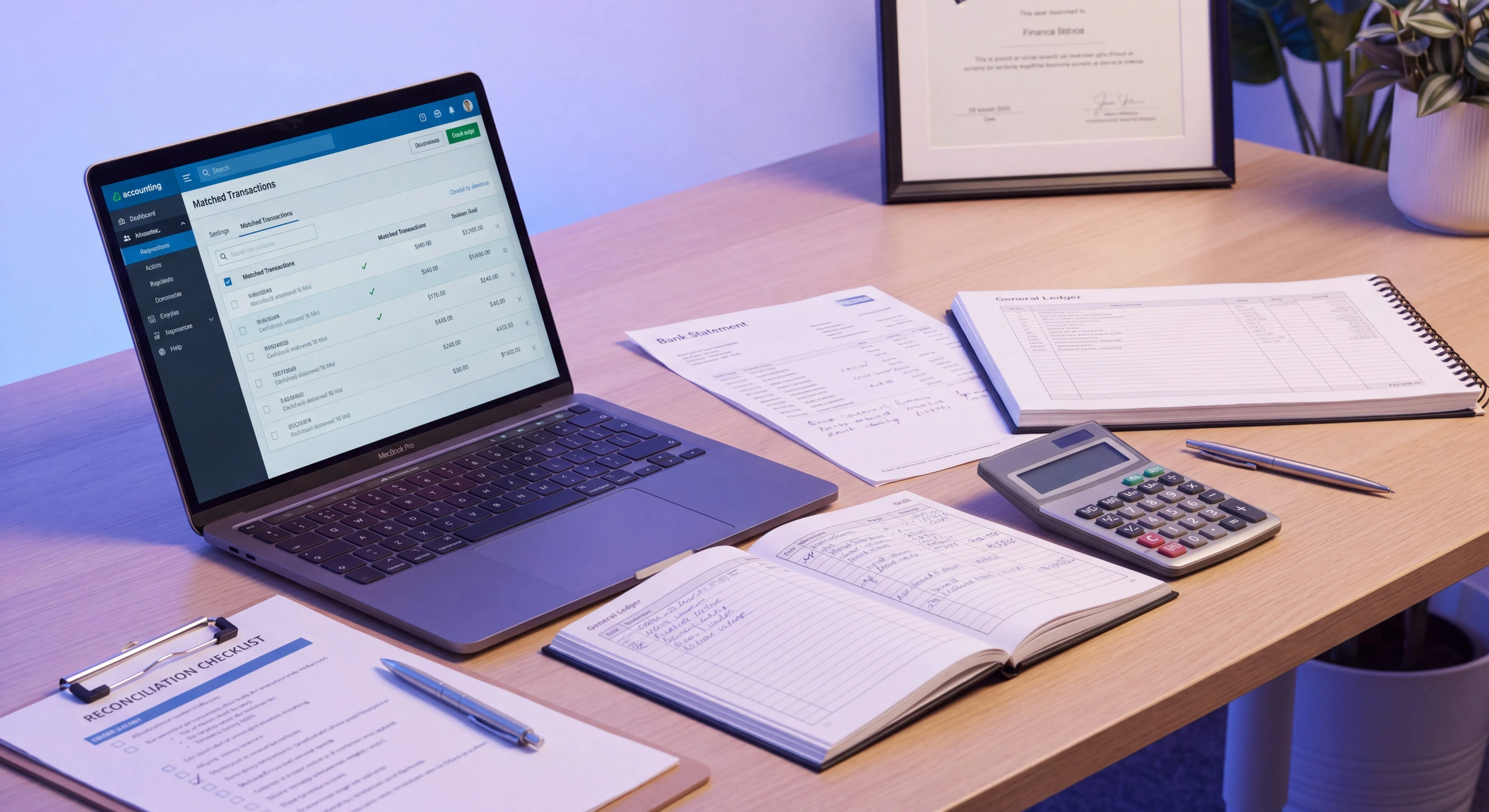

The first time I had a bookkeeper walk me through a bank reconciliation, I expected something complicated. It wasn’t. It was tedious, careful, and weirdly satisfying, like balancing a checkbook with the volume turned up.

What surprised me was the part that went wrong. She found a $1,240 difference between the bank statement and the books. It took her forty minutes to track it down. It was a duplicated vendor payment that nobody had caught for two weeks. Without that reconciliation, it would have sat there until something worse happened.

That’s the whole case for the bank reconciliation process in one story. It’s not busywork. It’s the control that catches the thing you didn’t know was wrong.

I’m Yuval, CEO of Glitter AI, and I spend a lot of time with finance and bookkeeping teams who want their reconciliations to be fast, accurate, and survivable when the person who normally does them is out. This is a step-by-step walkthrough of the bank reconciliation process, how to match transactions, how to chase down discrepancies, and how to write it all down once so you never re-train it from scratch.

Teach your co-workers or customers how to get stuff done – in seconds.

What Is the Bank Reconciliation Process?

The bank reconciliation process is the routine of comparing your accounting records against your bank statement to confirm every transaction matches and the ending balances agree. When they don’t agree, you dig into the difference until you can explain it.

In plain terms: the bank says you have one number, your books say you have another, and reconciliation is the work of proving they’re really the same number once timing and errors are accounted for.

It’s one of the most basic controls in the broader bookkeeping process. If you want the wider context, the glossary entry on standard operating procedures covers why repeatable processes like this matter and where reconciliation sits inside a finance function.

A good reconciliation answers three questions for the period:

- Does every bank transaction appear in the books? (nothing missing)

- Does every book transaction appear on the bank statement? (nothing fabricated or duplicated)

- Can you explain every difference between the two balances? (timing items, not errors)

Most reconciliations I see answer the first question, skim the second, and treat the third as “close enough.” That’s how a duplicated payment hides for two weeks.

Why Reconciling Your Bank Account Matters

Before we get to the steps, it’s worth being honest about why this earns a spot on your calendar.

- It catches errors and fraud. Duplicate payments, unauthorized withdrawals, and bank mistakes show up here first.

- It keeps your books trustworthy. Every step of the financial reporting process, from cash flow to month-end, inherits the accuracy of your reconciliation.

- It supports the audit trail. A clean reconciliation is documentary evidence; see the audit trail glossary entry for why that paper trail matters.

- It speeds up the close. Reconciling cash first makes the rest of the month-end close process far less painful.

The stakes are higher than many teams realize. According to the ACFE’s 2024 Report to the Nations, more than half of occupational fraud cases involve either a lack of internal controls (32% of cases) or management override of existing controls (19%). Account reconciliation is one of the few controls that can catch both. And when those controls are absent, the ACFE finds the median fraud scheme runs for 12 months before anyone notices.

Skip it, and the errors don’t disappear. They just compound until they’re expensive.

The Bank Reconciliation Process, Step by Step

Here’s the process I’d put in a written SOP for any bookkeeping team. Works the same whether you reconcile on paper, in a spreadsheet, or inside QuickBooks or Xero.

Step 1: Gather Your Documents

You can’t reconcile what you can’t see. Before you start, pull together:

- The bank statement for the period (or the bank feed if you’re working in software)

- The general ledger cash account or cash book for the same period

- The prior period’s reconciliation so you know your starting point

- Any outstanding items carried forward (uncleared checks, deposits in transit)

The single most common reason a reconciliation goes sideways? Starting from the wrong opening balance. Confirm that last period’s reconciled balance matches this period’s beginning balance before you do anything else.

Step 2: Match the Opening Balance

Compare the ending balance from your last reconciliation to the opening balance on the new bank statement. They should tie. If they don’t, stop and fix that before you move on. Everything after this step assumes a clean starting point.

Step 3: Match Transactions Line by Line

This is the heart of the work. Go through every transaction and match the bank statement to the books:

- Deposits and incoming payments - every deposit on the statement should have a matching entry in your books.

- Withdrawals, checks, and payments - every payment in your books should appear on the statement (or be a known outstanding item).

- Bank-only items - interest earned, bank fees, and automatic charges often appear on the statement but not yet in your books. These need to be recorded.

- Book-only items - checks you’ve written that haven’t cleared, and deposits in transit, appear in your books but not yet on the statement. These are timing differences, not errors.

Tick off each matched pair as you go. The unmatched items at the end are your investigation list.

Teach your co-workers or customers how to get stuff done – in seconds.

Step 4: Identify and Categorize Discrepancies

Anything that didn’t cleanly match falls into one of a few buckets, and naming the bucket tells you what to do next:

- Timing differences - outstanding checks and deposits in transit. No action beyond carrying them forward; they’ll clear next period.

- Bank-side items not yet booked - fees, interest, returned checks, automatic payments. Record these in your books.

- Errors in your books - transposed numbers, wrong amounts, missing entries, duplicates. Correct these with a journal entry or by fixing the original record.

- Bank errors - rare, but they happen. Document them and contact the bank.

The discipline here is to label every difference. “I don’t know what this is” is not a category; it’s a flag to keep digging.

Step 5: Investigate the Stubborn Differences

When the numbers still won’t agree, work through the usual suspects in order:

- Check the math. Re-add the outstanding items. A single transposed digit ($1,240 vs $1,420) explains a surprising share of differences.

- Look for duplicates. Search both sides for the same amount appearing twice.

- Check the dates. A transaction recorded in the wrong period looks like a discrepancy until you widen the date range.

- Reverse the sign. A payment booked as a deposit (or vice versa) creates a difference of exactly twice the amount.

- Compare to the prior reconciliation. A stale uncleared item from months ago may need to be voided or investigated.

Most differences resolve in the first two checks. The rest reward patience.

Step 6: Make Adjusting Entries

Once you understand a difference, fix it in the right place:

- Bank fees, interest, and charges → record as journal entries in your books.

- Errors in your records → correct the original transaction or post an adjusting entry.

- Genuine bank errors → leave your books correct, log the issue, and follow up with the bank.

Never adjust the bank statement to match your books. The statement is the independent record; your books move toward it, not the other way around.

Step 7: Confirm the Balances Agree

After adjustments, the reconciliation should balance: your adjusted book balance equals the bank statement balance plus deposits in transit minus outstanding checks. When that equation holds, the period is reconciled.

Step 8: Document and Sign Off

Save the completed reconciliation, the supporting statement, and a note on any unusual items. Have someone other than the preparer review it. This separation of duties is the part most small teams skip, and it’s exactly the part an auditor looks for. The accounts receivable SOP entry covers similar review discipline on the AR side.

How to Do Bank Reconciliation in QuickBooks

If you’re using QuickBooks Online, the mechanics are mostly built for you. The judgment still isn’t.

- Go to Settings → Reconcile and pick the bank account.

- Enter the ending balance and ending date from your bank statement.

- QuickBooks shows your transactions next to the statement period. Match the ones that clear; check them off.

- Watch the Difference field in the top corner. Your goal is to get it to $0.00.

- If the difference won’t zero out, use the discrepancy report to see what changed since the last reconciliation (deleted or edited transactions are a frequent culprit).

- Once the difference is zero, click Finish now.

The trap with QuickBooks is the bank feed. Auto-matched transactions feel reconciled but aren’t until you actually run the reconcile workflow. Don’t confuse “categorized in the feed” with “reconciled.”

How to Do Bank Reconciliation in Xero

Xero takes a continuous approach instead of a monthly batch.

- Open the bank account; Xero shows imported statement lines waiting to be reconciled.

- For each line, match it to an existing transaction or create the entry directly.

- Use suggested matches carefully - confirm the amount and date rather than clicking through.

- At period end, run the Bank Reconciliation report and confirm the statement balance equals the reconciled balance.

- Investigate anything in the unreconciled list before you call the period done.

Xero’s “reconcile as you go” model keeps the daily list short, but it still needs a true period-end check. Reconciling every line doesn’t guarantee the ending balance ties; the report does.

How Often Should You Reconcile?

Frequency depends on transaction volume and risk tolerance:

- Monthly is the standard for most small businesses, aligned to the bank statement cycle.

- Weekly suits businesses with high transaction volume or tight cash positions.

- Daily makes sense for retail, hospitality, or any operation with heavy cash handling and elevated fraud exposure.

The honest rule: reconcile often enough that an error can’t do real damage before you catch it. For most teams that’s monthly at minimum, and never less than that.

Write the Process Down Once

Here’s the part most teams miss. The bank reconciliation process above is knowable and repeatable, and almost always trapped in one person’s head. Ventana Research found that 72% of organizations that automate most or all of their reconciliations complete their quarterly close within six business days, compared to just 25% where reconciliation work is largely manual - a gap that traces directly back to whether the underlying process is documented and repeatable enough to systematize.

When that person is on vacation during close week, the reconciliation either doesn’t happen or gets done badly by someone guessing at the steps. I’ve watched it happen more times than I’d like.

This is the gap I built Glitter AI to close. Rather than writing a static document nobody reads, you record yourself doing the reconciliation once, talking through it as you go, and Glitter turns it into a clean step-by-step guide with screenshots. The next person follows the real process, in QuickBooks or Xero, exactly the way your best bookkeeper does it. For the bigger picture on documenting finance work, the month-end close process walkthrough goes deeper on closing the books around reconciliation.

A reconciliation process you can hand off is worth far more than one that only works when one specific person shows up.

Teach your co-workers or customers how to get stuff done – in seconds.

Frequently Asked Questions

What is the bank reconciliation process?

The bank reconciliation process is the routine of comparing your accounting records to your bank statement to confirm every transaction matches and the ending balances agree. When the balances differ, you investigate timing items and errors until every difference is explained.

What are the steps in a bank reconciliation?

The core steps are: gather your documents, match the opening balance, match transactions line by line, identify and categorize discrepancies, investigate stubborn differences, make adjusting entries, confirm the balances agree, and document and sign off. Each step narrows the gap between your books and the bank statement.

How do you do a bank reconciliation in QuickBooks?

In QuickBooks Online, go to Settings then Reconcile, select the account, enter the statement's ending balance and date, match cleared transactions until the Difference field reads $0.00, then click Finish now. If it won't zero out, use the discrepancy report to find edited or deleted transactions.

How is bank reconciliation done in Xero?

Xero reconciles continuously. You match or create an entry for each imported statement line, confirm suggested matches by amount and date, then run the Bank Reconciliation report at period end to verify the statement balance equals the reconciled balance and clear any unreconciled items.

How often should you reconcile your bank account?

Monthly is standard for most small businesses, aligned to the bank statement cycle. High-volume or cash-heavy businesses should reconcile weekly or daily. The rule of thumb is to reconcile often enough that an error can't cause real damage before you catch it.

What causes a bank reconciliation not to balance?

Common causes are outstanding checks and deposits in transit (timing differences), unrecorded bank fees or interest, transposed or duplicated amounts, transactions in the wrong period, and a payment booked with the wrong sign. Editing or deleting an already-reconciled transaction is a frequent culprit in software.

What is the difference between outstanding checks and deposits in transit?

Outstanding checks are payments you've recorded in your books but the bank hasn't cleared yet, so they reduce the book balance but not the bank balance. Deposits in transit are deposits you've recorded that haven't posted to the bank yet. Both are timing differences that resolve in a later period, not errors.

Should you adjust the bank statement or your books?

Always adjust your books, never the bank statement. The statement is the independent third-party record. You record bank-side items like fees and interest in your books and correct your own errors, but genuine bank errors are documented and raised with the bank rather than booked away.

Who should review a bank reconciliation?

Someone other than the person who prepared it should review and sign off. This separation of duties is a basic internal control that catches errors and reduces fraud risk, and it's exactly the evidence auditors look for in a clean reconciliation.

Can bank reconciliation be automated?

Matching can be largely automated by bank feeds in QuickBooks and Xero, but the judgment work, categorizing discrepancies, investigating differences, and signing off, still requires a person following a documented process. Automating the matching only helps if the surrounding process is written down and repeatable.