Read summarized version with

Last quarter I watched an FP&A lead spend her entire Friday rebuilding a board deck because someone had emailed her “the final numbers” twice, four hours apart, and the second version was the actual final one.

The model was fine. The narrative was fine. What broke was the part nobody calls a process: getting numbers out of the close, into a consolidated view, dressed up as statements, reviewed by the right people, and into the right hands without a single “wait, is this the latest one?”

That whole sequence is the financial reporting process. Most teams run it every month and almost none of them have it written down.

I’m Yuval, CEO of Glitter AI. A lot of my time goes to finance and FP&A teams who treat reporting as something that just happens after close, rather than a process with its own steps, owners, and ways to fail. So here’s a walkthrough. What the financial reporting process actually is, the five steps it moves through, and how to document it so it stops living in one person’s inbox.

Teach your co-workers or customers how to get stuff done – in seconds.

What Is the Financial Reporting Process?

The financial reporting process is the recurring set of steps a finance team uses to turn closed books into finished, reviewed financial reports and get them to the people who need them: leadership, the board, lenders, investors, and auditors.

Here’s the distinction people miss. The close produces correct numbers. Reporting produces a usable story those numbers tell. They’re adjacent, they overlap, and they’re not the same job. The financial close process ends when the period is locked. Reporting starts from that locked data and ends when a decision-maker is holding a statement they trust.

If your close is solid but your reporting is a scramble, you don’t have a close problem. You have an undocumented reporting process. That’s what this post is about.

The Five Steps of the Financial Reporting Process

Reporting is a sequence with dependencies, not a pile of tasks you can do in any order. It moves through five steps: data collection, consolidation, statement preparation, review, and distribution. Each one hands off cleanly to the next. Each one also has a classic way it goes wrong.

Step 1: Data Collection

Reporting starts the moment the books are closed, by pulling the source data: the trial balance, the general ledger detail, subledger reports, and any operational data the report needs (headcount, units, bookings, whatever your KPIs run on).

The single most common failure here is starting before the period is actually locked. If you build reports off a trial balance that’s still moving, every downstream step inherits the drift. The rule is simple: reporting consumes a locked period, not a live one. This is exactly why the general ledger process and reporting need a hard boundary between them, not a blurry one.

Practical things to nail down in this step:

- A single, named source for the trial balance (one system, one export, one timestamp)

- A defined cutoff: reporting uses the data as of close lock, not “whatever’s in there now”

- Non-financial inputs collected and dated the same way financial ones are

Step 2: Consolidation

One legal entity, one currency? Consolidation is light. Run multiple entities, currencies, or business units, and this is where the real work lives.

Consolidation is where you combine entity-level trial balances into a single group view: eliminating intercompany transactions, translating foreign currencies, and rolling subsidiaries up into the parent. The output is one consolidated set of balances everyone agrees is the numbers.

The failure mode here is intercompany. Entity A booked the charge, Entity B never booked the matching side, and the elimination doesn’t net to zero. Catch that at consolidation and it costs you almost nothing. Catch it after the board deck is printed and it costs you a lot. Treat intercompany tie-out as a control, not a courtesy check, the same way you’d treat any other financial control.

Step 3: Statement Preparation

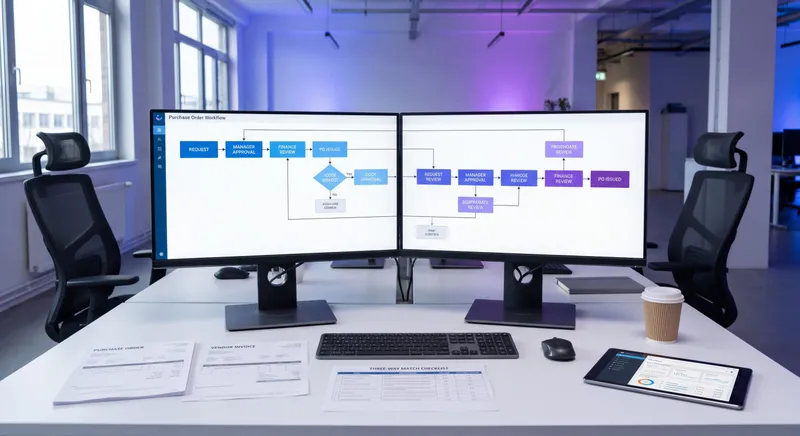

Now you build the actual outputs. For most teams that’s the big three: the income statement, the balance sheet, and the cash flow statement, plus whatever management reporting package leadership actually reads (a KPI summary, departmental P&Ls, a budget-vs-actual view).

Two things matter most in this step.

First, the statements have to tie to each other. Net income flows to retained earnings on the balance sheet. The cash flow statement reconciles to the change in the cash balance. If they don’t tie, the report isn’t done, it just looks done.

Second, the management package is usually more politically loaded than the GAAP statements. Budget-vs-actual variances are where the questions get asked, so the comparison basis (which budget version, which prior period) needs to be defined and consistent, not re-picked every month. If you’re comparing against budget, the budgeting process and the reporting process need to agree on what “budget” even means.

Teach your co-workers or customers how to get stuff done – in seconds.

Step 4: Review

This is the step teams compress when they’re behind, and it’s the one they shouldn’t. An EY Closing Excellence survey found that top-performing organizations complete monthly reports in 6 working days versus 12 for average companies - a difference that traces largely to disciplined, structured review rather than faster accounting work.

Review is a structured second look before anything leaves the building: a flux/variance analysis against prior period and budget, a tie-out check across statements, and a sign-off by someone who is not the person who prepared the reports. The reviewer’s job isn’t to re-do the math. It’s to ask “does this story make sense, and can we defend every number that moved?”

A few non-negotiables in review:

- Preparer ≠ reviewer. If the same person builds and approves the reporting package, you don’t have a review, you have a formality. This is the same segregation-of-duties logic that runs through every internal control in accounting.

- Variances get explanations, not just identification. “Marketing is up 18%” is an observation. “Marketing is up 18% because the conference spend that slipped from Q1 landed this month” is review.

- One version is blessed. The moment review is done, that package is the package. Everything else is a draft and should be labeled like one.

The version problem is worth dwelling on, because it’s where reporting most often embarrasses people. A documented review step with a clear “this is final” gate is the cheapest insurance you can buy against the Friday-afternoon rebuild.

Step 5: Distribution

The last step is getting the blessed package to the right audience, in the right format, on schedule, with a clear record of what was sent.

Distribution sounds trivial until you actually map it. Different audiences need different cuts. The board gets a deck and commentary. Lenders get specific covenant calculations. Department heads get their own P&L and not everyone else’s. Auditors get the full package plus support. Each of those is a different deliverable from the same blessed source.

The thing to protect here is the link between distribution and the locked, reviewed package. Every report that goes out should be traceable back to a specific reviewed version, on a specific date, sent to a specific list. That traceability is your audit trail in practice, and it’s what lets you answer “which numbers did the board actually see in March?” without a forensic email search.

Where the Financial Reporting Process Actually Breaks

After watching a lot of these run, the failures cluster in the same few places. According to Ventana Research, only about 31% of organizations automate most or all of their reconciliations, which means the data feeding the reporting process is still largely produced by hand at most companies. That manual foundation is where version confusion, timing errors, and unexplained variances originate - and why the failures below are so persistent.

- Starting before the period is locked. Reporting on a moving target. Everything downstream inherits the drift.

- Intercompany not netting to zero. A consolidation problem discovered after distribution instead of before.

- Statements that don’t tie. Especially cash flow not reconciling to the cash balance change.

- Skipped or rubber-stamp review. No real second set of eyes, so errors and unexplained variances go out the door.

- Version chaos. Multiple “finals” in flight because there’s no single blessed package and no clear gate.

- Untraceable distribution. Nobody can say with certainty which version a given stakeholder received.

Notice that none of these are accounting errors. They’re process errors. The numbers are usually right. The process around the numbers is what fails.

Document It Once So It Survives the People Who Run It

Here’s the uncomfortable truth. For most teams, the financial reporting process doesn’t live in a system. It lives in one analyst’s head and one analyst’s file structure. Which tab the consolidation pulls from. Which budget version is “the real one.” Which board member always asks about gross margin so that slide had better be bulletproof. Which folder the final-final deck goes in.

That works right up until that analyst is out during reporting week, or leaves. Then the reporting process, the thing leadership and the board lean on to make decisions, walks out the door with them. The close survives because it’s at least somewhat systematized. Reporting often doesn’t, because it’s the part everyone assumes is “just pulling the numbers together.”

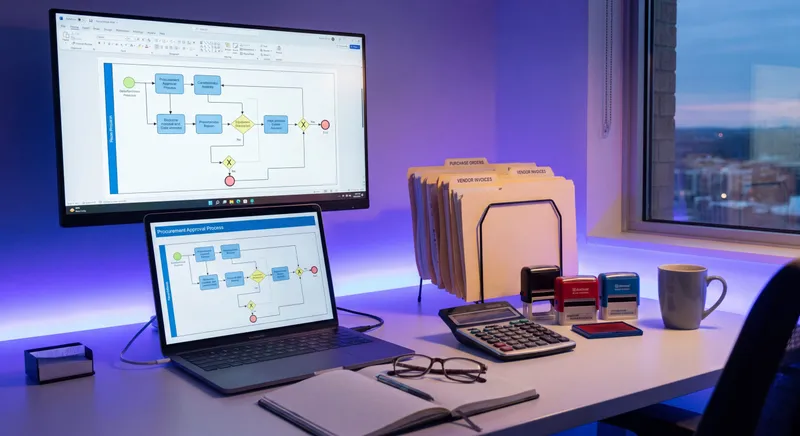

That’s the problem I built Glitter AI to solve. Instead of writing a reporting manual nobody updates, you click through your actual reporting process one time, the trial balance export, the consolidation workbook, the statement build, the review checklist, the distribution list, in your real systems, and Glitter turns it into a clean, visual, step-by-step guide with screenshots, automatically. Next month, whoever runs reporting follows the guide instead of reverse-engineering the last analyst’s folders. When the process changes, you re-record the one step that changed instead of rewriting a document.

A documented reporting process is the difference between a repeatable monthly cycle and a single point of failure that happens to have worked so far. For the broader pattern of standardizing finance work this way, the month-end close process walkthrough is a good companion to this one.

Teach your co-workers or customers how to get stuff done – in seconds.

A Quick Playbook

If you want to tighten your financial reporting process starting this cycle, do these four things in order:

- Draw a hard line between close and reporting. Reporting consumes a locked period. If close isn’t locked, reporting hasn’t started.

- Make intercompany tie-out and statement tie-out explicit checks, with a named owner, not assumptions.

- Make review real: preparer ≠ reviewer, variances explained, one blessed version.

- Record the reporting process once as a visual guide so next cycle doesn’t depend on the same analyst being at their desk.

None of this requires software you don’t already have. It just requires the reporting process to exist somewhere other than one person’s file structure.

Frequently Asked Questions

What is the financial reporting process?

The financial reporting process is the recurring set of steps a finance team uses to turn closed books into finished, reviewed financial reports and deliver them to stakeholders. It moves through data collection, consolidation, statement preparation, review, and distribution.

What are the steps in the financial reporting process?

There are five core steps: collecting source data from a locked period, consolidating entity-level data into a group view, preparing the financial statements and management package, reviewing with a variance analysis and independent sign-off, and distributing the blessed package to each audience.

How is financial reporting different from the financial close?

The financial close produces correct, locked numbers for a period. Financial reporting starts from that locked data and produces reviewed, usable reports for decision-makers. They are adjacent and overlapping but separate processes with different owners and failure modes.

Why should reporting only start after the period is locked?

If you build reports from a trial balance that is still changing, every downstream step inherits that drift. Reporting should consume a locked period, not a live one, so the consolidated numbers and statements stay internally consistent.

What happens during the consolidation step?

Consolidation combines entity-level trial balances into a single group view by eliminating intercompany transactions, translating foreign currencies, and rolling subsidiaries into the parent. The most common failure is intercompany not netting to zero, which should be caught here as a control.

What does the review step in financial reporting involve?

Review is a structured second look before anything is distributed: a flux or variance analysis against prior period and budget, a tie-out check across statements, and sign-off by someone other than the preparer. Variances should be explained, not just identified.

Why do financial statements need to tie to each other?

Net income flows to retained earnings on the balance sheet, and the cash flow statement reconciles to the change in the cash balance. If the statements do not tie, the report only looks finished; tying them out is part of statement preparation, not an optional check.

Who should the financial reporting package be distributed to?

Different audiences need different cuts of the same blessed source: the board gets a deck and commentary, lenders get covenant calculations, department heads get their own P&L, and auditors get the full package plus support. Every distributed report should trace back to a specific reviewed version.

What is the most common reason the financial reporting process fails?

Most failures are process errors, not accounting errors: starting before the period is locked, intercompany not eliminating, statements that do not tie, skipped review, version chaos, and untraceable distribution. The numbers are usually right; the process around them is what breaks.

How do you document a financial reporting process?

The most durable approach is to capture the process as a visual, step-by-step guide recorded from the real systems and steps, rather than a static manual nobody updates. Tools like Glitter AI generate this automatically by recording the process once, so reporting survives turnover and vacations.