Read summarized version with

The first time I tried to automate accounting at a startup, I made it worse.

I bought a tool, wired it up to our bank feed, and felt pretty smart for about a week. Then our controller went on leave. Nobody else knew which rules she’d set up. Nobody knew why certain invoices auto-coded the way they did, or what to do when the automation got something wrong. We’d automated the work but lost track of how it actually worked. That’s worse than doing it by hand, honestly, because manual work is at least visible.

I’m Yuval, founder of Glitter AI. I’ve run finance for small companies the hard way, and I’ve watched plenty of finance leaders repeat the mistake I made: treating accounting automation as a software purchase instead of a process you have to design, document, and own.

This guide is the version I wish someone had handed me back then. What’s actually worth automating, which tools matter, the ROI math your CFO will ask about, and the part almost everyone skips: documenting the automated workflows so they don’t turn into a black box.

Teach your co-workers or customers how to get stuff done – in seconds.

What “accounting automation” actually means

Let’s get the definition straight, because vendors blur it on purpose.

Accounting automation is using software to handle repetitive, rules-based finance tasks that used to require manual data entry, matching, or routing. It’s not AI doing your judgment for you. It strips out the keystrokes and the chasing so your team can spend time on the parts that actually need a brain.

If you want the textbook framing, our glossary breaks down process automation and the broader idea of workflow automation. But here’s the practical test I use: if a task has clear rules, happens often, and a person mostly copies data from one place to another, it’s a candidate. If the task needs judgment about an exception or a relationship, it isn’t, at least not fully.

The goal isn’t a finance team of zero people. It’s a finance team that isn’t drowning in invoices and reconciliations, so they can actually do analysis, controls, and forecasting.

What to automate (and in what order)

Don’t automate everything at once. I’ve watched teams try, and end up with five half-working integrations nobody trusts. Go in this order. It roughly tracks effort to payoff.

1. Accounts payable (start here)

AP is the highest-volume, most repetitive thing most finance teams do, which makes it the best first win. According to APQC benchmarking data, the median cost to process a single AP invoice is about $5.83 - but top-quartile teams bring that down to $2.07 or less. That gap is almost entirely explained by automation. Modern AP automation handles:

- Invoice capture - OCR pulls vendor, amount, date, and line items from PDFs and emails so nobody types them.

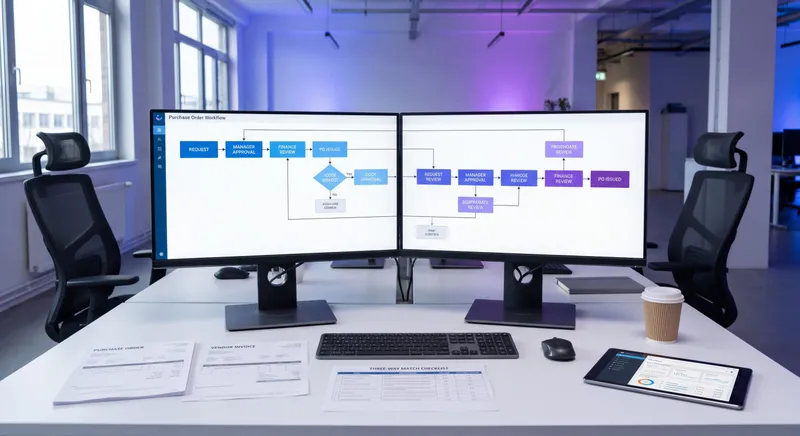

- Three-way matching - the system matches the invoice to the purchase order and the receipt automatically. If you’ve never formalized this, read up on three-way match first, because automating a process you haven’t defined just automates the chaos.

- Approval routing - invoices over a threshold route to the right approver by rule, with reminders, instead of you forwarding emails around.

- Payment runs - scheduled batches with built-in controls.

If you only automate one thing this quarter, make it AP. It’s also where most fraud and duplicate-payment risk lives, so the controls tend to pay for themselves.

2. Accounts receivable and cash application

On the AR side, the painful but automatable parts are invoice delivery, payment reminders, and matching incoming payments to open invoices, the work known as cash application. Automating reminders alone usually pulls days off your DSO, because customers pay when they’re nudged consistently and unemotionally.

3. Expense management

Receipt capture, policy checks, and reimbursement routing. The ROI here is less about hard dollars and more about ending the end-of-month expense report misery and catching policy violations before they’re paid, not after.

4. Reconciliations

Bank, credit card, and intercompany reconciliations are rules-heavy and high-volume, which makes them great for automation. Just do it after AP and AR are clean, since reconciliation quality depends on the data feeding it. Auto-matching clears the 90% of transactions that obviously match, so your team only looks at the genuine exceptions.

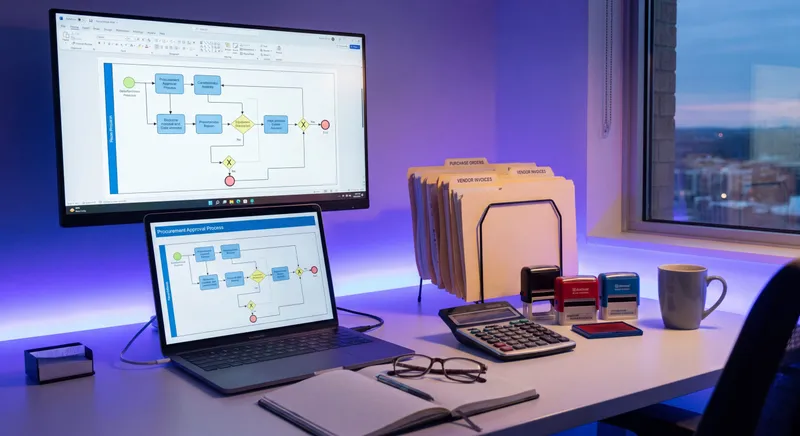

5. The month-end close

The close is the boss level. It isn’t one task. It’s dozens of interdependent tasks with handoffs between them. You don’t “buy close automation”; you automate the pieces (reconciliations, accruals, flux analysis, the close checklist itself) and orchestrate them. Teams that do this well shave days off the close, every single month, forever. To put a number on the current baseline: a 2025 month-end close benchmark by Ledge found that half of finance teams still take more than five business days to close, and only 18% manage to close in three days or less.

Teach your co-workers or customers how to get stuff done – in seconds.

The tools, honestly

I’m not going to pretend there’s one tool. There isn’t, and anyone who tells you otherwise is selling something. Here’s how the landscape actually breaks down:

- Your ERP or accounting platform (QuickBooks, Xero, NetSuite, Sage). Start by turning on the automation you’re already paying for. Bank rules, recurring transactions, and approval workflows are usually built in and sitting unused.

- AP/AR specialists (Bill, Stampli, Tipalti, Melio, and similar). These do one thing deeply. Worth it once your volume justifies a dedicated tool.

- Close and reconciliation platforms (FloQast, Numeric, Blackline-style tools). For teams where the close is genuinely a multi-person, multi-day project.

- Expense tools (Ramp, Brex, Expensify-style). Often bundled with corporate cards, which is where most of the real automation payoff comes from.

- Glue (native integrations, iPaaS, or light scripting). The unglamorous layer that makes the others talk to each other. Budget time for it.

My advice: wring out your existing platform’s built-in automation before buying anything. I’ve watched companies pay for a shiny AP tool while three approval-routing features sat switched off in their ERP.

The ROI math your CFO will ask for

Don’t pitch automation as “it’ll save time.” Quantify it. Here’s the framework I use.

Hard costs avoided. Take a task, say AP invoice processing. Estimate minutes per invoice done manually (data entry + matching + routing). Multiply by monthly volume, then by loaded hourly cost. A team processing 800 invoices a month at 9 minutes each is spending ~120 hours monthly. That’s most of a full-time person.

Error and leakage reduction. Duplicate payments, missed early-payment discounts, late fees, fraud. For a lot of mid-size companies this quietly runs into five or six figures a year. Recovering early-payment discounts alone often funds the tooling by itself.

Cycle-time value. A faster close means you make decisions on real numbers sooner. Lower DSO means cash in the door earlier. These don’t show up as a line item, but they’re real.

Cost to subtract. Software, implementation time, and ongoing maintenance. Be honest about implementation. It’s always more than the demo suggests.

If the annual avoided cost plus leakage reduction doesn’t clear 2-3x the all-in tool cost in year one, either the process volume is too low or you’re automating the wrong thing. Move down the priority list.

The part everyone skips: document the automated workflow

Here’s the mistake I made, and the reason I’m writing this post.

When you automate a process, the knowledge of how it works doesn’t disappear. It just moves. It moves into rules, mappings, thresholds, and integration settings inside a tool that maybe two people understand. When those two people leave, you don’t have an efficient finance function. You have a black box that nobody can fix, audit, or change.

Automation without documentation is a single point of failure with extra steps.

So every automated workflow needs a living document that captures:

- The trigger and the rules. What kicks it off, and the actual logic: approval thresholds, coding rules, matching tolerances. The real numbers, not “it routes to the manager.”

- The exception path. What a human does when the automation can’t decide. This is the most important part, and the most undocumented one.

- The system map. Which tools touch the data and in what order, so a broken integration is debuggable.

- The owner. A named person responsible for the rules, not “finance.”

This is exactly the gap I built Glitter AI to close. You run through the automated workflow once, clicking through the AP tool, showing the approval rules, walking the exception handling, talking out loud as you go. Glitter captures the screen and your narration and turns it into a clean step-by-step guide with screenshots. It’s SOP capture for the work your software now does, so the why survives even though the doing is automated.

For the underlying finance procedures themselves, I’ve written a full accounting SOP guide. There’s also a deep dive on the accounts payable SOP. Automate the steps in those, but document them first.

Teach your co-workers or customers how to get stuff done – in seconds.

A 90-day rollout that actually works

If I were starting today, here’s the plan.

Days 1-30: Pick one process and document the manual version. Almost always AP. Map it the way it really runs today, exceptions included. You can’t automate a process you can’t describe.

Days 31-60: Automate the obvious 80%. Turn on capture, matching, and routing. Deliberately leave the messy 20% manual for now. Build the audit trail into the workflow from day one. Automation that can’t be audited will fail you in your next review.

Days 61-90: Document the automated workflow and assign an owner. Record the new process, including the exception path, and put a name on it. Then measure: invoices per hour, exception rate, cycle time. Compare that to your day-1 baseline. The delta is your ROI story for the next process.

Then repeat the loop with AR, expenses, reconciliations, and finally the close.

The mindset shift

The finance leaders who get automation right don’t think of it as buying software. They think of it as redesigning processes, then having software run the parts that don’t need a person.

The tooling is the easy 30%. The hard 70% is deciding what to automate, designing the exception handling, and documenting it so the automation becomes an asset your team owns rather than a black box your team fears. McKinsey estimates that currently available technology can fully automate an estimated 42% of finance activities and mostly automate a further 19% - but the bottleneck was never the software.

Get that order right and accounting automation does what it’s supposed to: it gives your team back the hours they were burning on keystrokes, so they can spend them on the work that actually moves the company.

Frequently Asked Questions

What is accounting automation?

Accounting automation is using software to perform repetitive, rules-based finance tasks like invoice data entry, three-way matching, payment routing, and reconciliations. It removes manual keystrokes and chasing so finance teams can focus on analysis, controls, and judgment-based work.

What accounting processes should I automate first?

Start with accounts payable. It is high-volume, highly repetitive, and carries the most duplicate-payment and fraud risk, so it delivers the fastest payback. From there, move to accounts receivable and cash application, expense management, reconciliations, and finally the month-end close.

How much does accounting automation save?

It varies by volume, but a team processing 800 invoices a month manually can spend roughly 120 hours monthly on AP alone. Combined with reduced duplicate payments, recovered early-payment discounts, and fewer late fees, the avoided cost often clears 2-3x the tool cost in year one.

What are the best accounting automation tools?

There is no single tool. Start with the automation already built into your ERP or accounting platform (QuickBooks, Xero, NetSuite, Sage), then add AP/AR specialists, close and reconciliation platforms, or expense tools as volume justifies them. Exhaust your existing platform's features before buying new software.

Can you automate the month-end close?

Not as a single purchase. The close is dozens of interdependent tasks. You automate the components - reconciliations, accruals, flux analysis, and the close checklist itself - and orchestrate them. Teams that do this well consistently shave days off every close.

Why is documenting automated accounting workflows important?

When you automate a process, the knowledge of how it works moves into rules and settings inside a tool only a few people understand. Without documentation, that becomes a single point of failure that nobody can audit, fix, or change when those people leave.

What should documentation of an automated workflow include?

It should capture the trigger and the actual rules (approval thresholds, coding logic, matching tolerances), the exception path a human follows when automation can't decide, the system map showing which tools touch the data, and a named owner responsible for the rules.

Does accounting automation replace accountants?

No. The goal is not a finance team of zero people. It removes repetitive data entry and chasing so the existing team can spend time on analysis, controls, forecasting, and exception handling - the work that actually requires judgment.

How do I calculate the ROI of accounting automation?

Estimate manual minutes per task times monthly volume times loaded hourly cost to get hard cost avoided. Add error and leakage reduction (duplicate payments, missed discounts, late fees) and cycle-time value (faster close, lower DSO). Subtract software, implementation, and maintenance costs.

What is the risk of automating accounting without documentation?

Automation without documentation is a single point of failure with extra steps. The process becomes a black box: when the people who configured it leave, nobody can audit it, debug a broken integration, adjust the rules, or pass a control review.