Read summarized version with

A few years ago I sat with the controller of a fast-growing services company who told me her cash flow problem wasn’t a sales problem. It was a receivables problem.

They were closing deals fine. The money just wasn’t coming in. Invoices went out late, nobody owned collections, and payments landed in the bank with no idea which customer they belonged to. According to Atradius, an estimated 43% of credit-based B2B sales in the US are currently overdue - a reminder that late payment is the default state for a lot of customers, not the exception. By the time someone noticed an account was 90 days past due, the relationship had already gone cold.

Here’s the thing. The accounts receivable process is the part of the business that turns “we made a sale” into “we have cash in the bank.” When it runs well, you don’t notice it. When it doesn’t, you feel it everywhere: in the bank balance, in the awkward customer calls, in the month-end scramble.

I’m Yuval, CEO of Glitter AI. I work with finance teams who are trying to make their AR process repeatable so it doesn’t live in one person’s head. This post walks the whole process step by step, the way I’ve seen it actually work.

Teach your co-workers or customers how to get stuff done – in seconds.

What Is the Accounts Receivable Process?

The accounts receivable process is the full set of steps a company uses to extend credit to a customer, bill them, collect payment, and record the cash. It starts before the first invoice ever goes out. It doesn’t end until the money is matched against the right account and reported.

Most people think AR is just “send invoice, wait for check.” It isn’t. Teams that get paid on time treat AR as five connected stages, each with an owner and a clear hand-off.

For a quick definitional reference, the accounts receivable SOP glossary entry covers the standardized-procedure side of this. This post is the walkthrough.

Here are the five stages:

- Credit approval - deciding who gets to owe you money, and how much

- Invoicing - billing accurately and fast

- Collections - following up before things go bad

- Cash application - matching incoming money to open invoices

- Reporting - knowing where you stand and what to fix

Let’s walk each one.

Step 1: Credit Approval

Everything downstream gets easier or harder based on this step. If you extend generous terms to a customer who can’t pay, no amount of polite collections follow-up will fix that.

Before you onboard a new customer, the AR or credit function should:

- Run a credit check or pull a credit report for larger accounts

- Set a credit limit based on their financials and your risk tolerance

- Define payment terms (Net 30, Net 60, deposit required, etc.)

- Get the terms in writing on a signed order or contract

The mistake I see most often is treating this as a sales formality. Sales wants the deal closed, so credit terms get rubber-stamped. Then six months later AR is chasing a customer who was never a good credit risk in the first place.

Write down your credit policy and the thresholds that trigger a deeper review. That single document prevents most of the bad debt you’d otherwise eat later.

Step 2: Invoicing

You can’t collect on an invoice you never sent. You’d be surprised how often that’s the actual root cause of slow cash.

A clean invoicing step looks like this:

- The sale or delivery is confirmed (goods shipped, service rendered, milestone hit)

- AR generates the invoice promptly, ideally same-day

- The invoice includes everything the customer needs to pay: PO number, line items, terms, due date, remittance instructions

- The invoice goes to the right contact - not a generic inbox nobody checks

- It’s logged in your AR ledger so it shows up on the aging report

Two details matter more than people think. First, speed. An invoice sent five days late is a payment received five days late, every single time. Second, accuracy. A wrong PO number or a missing line item hands the customer a legitimate reason to sit on it. Now you’re in a dispute cycle instead of a payment cycle.

Teach your co-workers or customers how to get stuff done – in seconds.

Step 3: Collections

Collections is where most AR processes quietly fall apart, because it’s the step nobody wants to own. It feels confrontational. So it gets skipped until an account is severely past due, which is exactly when it’s hardest to recover.

The fix isn’t being more aggressive. It’s being more systematic. A good collections cadence is mostly automated and starts before the invoice is even late:

- Invoice date: confirmation the invoice was received

- A few days before due: a friendly reminder

- Due date: a clear “this is due today” note

- 7 days past due: a firmer follow-up, usually a call

- 30 days past due: escalation to a manager, possible credit hold

- 60+ days past due: formal escalation, payment plan, or collections agency

The point of the cadence is that nobody has to decide to follow up. The process decides. That’s also what makes collections trainable. A new AR hire can run the playbook on day one instead of learning who to chase by feel over six months.

This is the part of AR that benefits most from being documented step by step, since it’s both repetitive and high-stakes. A close cousin on the payables side is the accounts payable process, same principle, opposite direction of cash.

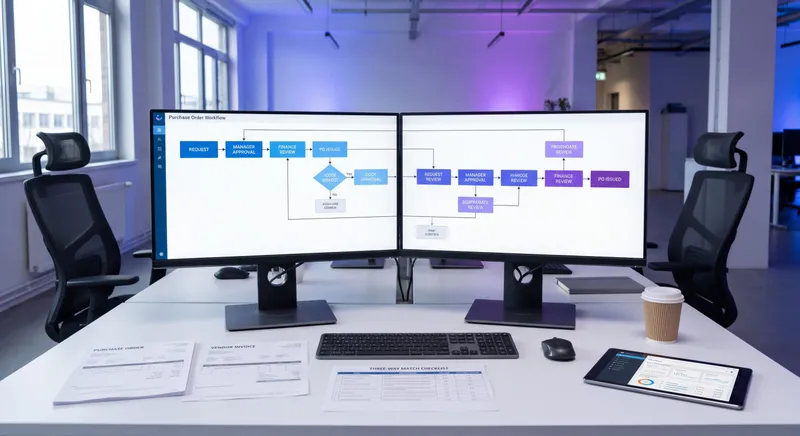

Step 4: Cash Application

Money comes in. Now you have to figure out which invoice it pays. This is cash application, and it’s the step that silently creates the most month-end pain.

A customer wires a payment with no remittance detail. Or pays three invoices with one check minus a deduction nobody documented. Or short-pays and you don’t know why. Every one of those becomes “unapplied cash” - money in the bank that your AR ledger still shows as owed.

The cash application step should:

- Pull the day’s receipts (lockbox, ACH, wire, card)

- Match each payment to one or more open invoices

- Handle deductions, short pays, and overpayments with a documented reason code

- Post the cash and close out the matched invoices

- Flag anything unmatched for same-day research, not month-end

I won’t go deep here because it deserves its own treatment. The cash application glossary entry covers the matching steps, the common failure modes, and why unapplied cash is so corrosive. The one rule worth repeating: chase unmatched payments the day they land, not the day you close the books.

Step 5: Reporting

The last step is knowing where you actually stand, so you can fix the process instead of just reacting to it.

The reports every AR function should run on a regular cadence:

- AR aging report - open balances bucketed by 0-30, 31-60, 61-90, 90+ days. This is your early warning system.

- DSO (Days Sales Outstanding) - on average, how long it takes to get paid. Trend it month over month.

- Collections effectiveness - how much of what was due actually came in

- Bad debt / write-offs - what you’ve given up on, and the credit decisions that led there

Reporting closes the loop. A creeping DSO points you back at invoicing speed or collections cadence. A spike in 90+ day balances points back at credit approval. The numbers tell you which of the earlier four steps is leaking. That’s the whole point of measuring them. For context on what good looks like: best-in-class AR teams consistently maintain lower DSO by pairing a systematic collections cadence with same-day cash application rather than treating either as discretionary work.

Why You Should Document the Whole Process Once

Here’s the pattern I see over and over. The AR process works fine - because one person knows it cold. They know which customer always disputes the first invoice, which one needs the PO on line one, which payment always arrives short by the freight charge. None of it is written down, not even on a basic bookkeeping checklist.

Then that person goes on vacation, or leaves, and cash flow drops off a cliff for a quarter while someone reverse-engineers it all without even a documented bookkeeping process to fall back on.

The accounts receivable process is the perfect thing to document once and reuse, since it’s repetitive, sequential, and high-stakes. That’s exactly why I built Glitter AI. You walk through your AR workflow once (credit check, invoicing, the collections cadence, cash application in your ERP) and Glitter turns it into a clean step-by-step guide with screenshots, automatically. The next AR hire follows the guide instead of shadowing someone for two months.

If you want the broader finance-department picture beyond AR, my guide to standardizing the whole accounting team covers how all of these procedures fit together, including structure and ownership for an accounting department. If your team runs on QuickBooks, it’s worth turning your QuickBooks workflow into documented SOPs so the AR steps survive turnover too.

Teach your co-workers or customers how to get stuff done – in seconds.

A Quick Recap

The accounts receivable process, end to end:

- Credit approval - vet the customer before you extend terms

- Invoicing - bill fast and accurately, log it immediately

- Collections - run a fixed cadence so follow-up isn’t a decision

- Cash application - match money to invoices the same day

- Reporting - measure DSO and aging to find the leak

Get those five running cleanly and AR stops being the reason cash is tight. Document them once and it stops being the reason you can’t take a vacation.

Frequently Asked Questions

What are the steps in the accounts receivable process?

The accounts receivable process has five core steps: credit approval (vetting the customer and setting terms), invoicing (billing accurately and promptly), collections (a structured follow-up cadence), cash application (matching incoming payments to open invoices), and reporting (tracking aging and DSO). Each step has an owner and a clear hand-off to the next.

What is the accounts receivable process?

The accounts receivable process is the end-to-end set of steps a company uses to extend credit, bill customers, collect payment, and record the cash received. It turns a completed sale into cash in the bank and typically spans credit approval through to reporting.

What is the difference between the accounts receivable and accounts payable process?

Accounts receivable is money owed to your company by customers, so the process focuses on invoicing and collecting. Accounts payable is money your company owes to vendors, so that process focuses on receiving and paying invoices. They are mirror images: AR brings cash in, AP sends cash out.

What is cash application in accounts receivable?

Cash application is the step of matching incoming customer payments to the correct open invoices, then posting the cash and closing those invoices. Poor cash application creates unapplied cash, where money is in the bank but the AR ledger still shows it as owed.

How can I speed up the accounts receivable process?

The fastest wins are invoicing same-day instead of in batches, running an automated collections cadence that starts before invoices are due, and applying cash the day it lands rather than at month-end. Speeding up invoicing alone often shaves days off DSO.

What is DSO in the accounts receivable process?

DSO, or Days Sales Outstanding, measures the average number of days it takes to collect payment after a sale. Tracking DSO month over month tells you whether your AR process is improving or degrading and which step is causing delays.

Who owns the accounts receivable process?

AR is usually owned by a finance or accounting team, often a dedicated AR specialist or credit and collections function. In smaller companies it may sit with a controller or bookkeeper. The key is that each step, especially collections, has a clearly assigned owner.

What is an AR aging report?

An AR aging report lists all open customer balances bucketed by how overdue they are, typically 0-30, 31-60, 61-90, and 90+ days. It is the primary early-warning tool for spotting accounts that need collections attention before they become bad debt.

Why is credit approval part of the accounts receivable process?

Credit approval is the first step because everything downstream depends on it. Extending generous terms to a customer who cannot pay guarantees collections problems and bad debt later. A documented credit policy with clear limits and terms prevents most avoidable losses.

How do I document the accounts receivable process so it survives turnover?

Document each of the five steps once as a step-by-step procedure with screenshots of your actual ERP or accounting system, including edge cases like disputes and short pays. Tools like Glitter AI capture the workflow as you perform it so a new hire can follow the guide instead of shadowing someone for months.