Read summarized version with

A few months ago I sat in on a call where a finance lead and a new controller spent twenty minutes arguing about whether the books were “closed.”

The numbers weren’t the issue. What “closed” actually meant was. One of them meant the bank rec is done and management can see directional numbers. The other meant every accrual is booked, every subledger ties out, and nobody touches this period again.

Both of them were right. They were just describing two different things, a soft close and a hard close, without anyone ever having written down which one the company actually runs.

I’m Yuval, CEO of Glitter AI. I spend a lot of time with finance teams who quietly carry this kind of ambiguity around in their heads. So here’s a walkthrough of the financial close process: what it actually is, how a hard close differs from a soft close, the timeline it should follow, the controls that keep it honest, and how it’s different from the month-end close most people picture when they hear the word “close.”

Teach your co-workers or customers how to get stuff done – in seconds.

What Is the Financial Close Process?

The financial close process is the recurring set of steps a finance team works through to finalize the books for a period and produce reliable financial statements. You record outstanding transactions, reconcile accounts, book adjusting entries, review the results, lock the period, and hand clean numbers to whoever needs them: leadership, the board, lenders, or auditors.

Here’s the distinction people miss. “Financial close” is the umbrella. “Month-end close” is one instance of it. Every month you run a close. Every quarter you run a heavier one. At year-end you run the heaviest one of all, the one the auditors care about. Same backbone in each case, but the depth and the controls scale up as the stakes go up.

If you want the step-by-step mechanics of the monthly version specifically, I wrote a dedicated month-end close process walkthrough with a companion checklist. This post stays one level higher: the shape of the close, regardless of which period you’re closing.

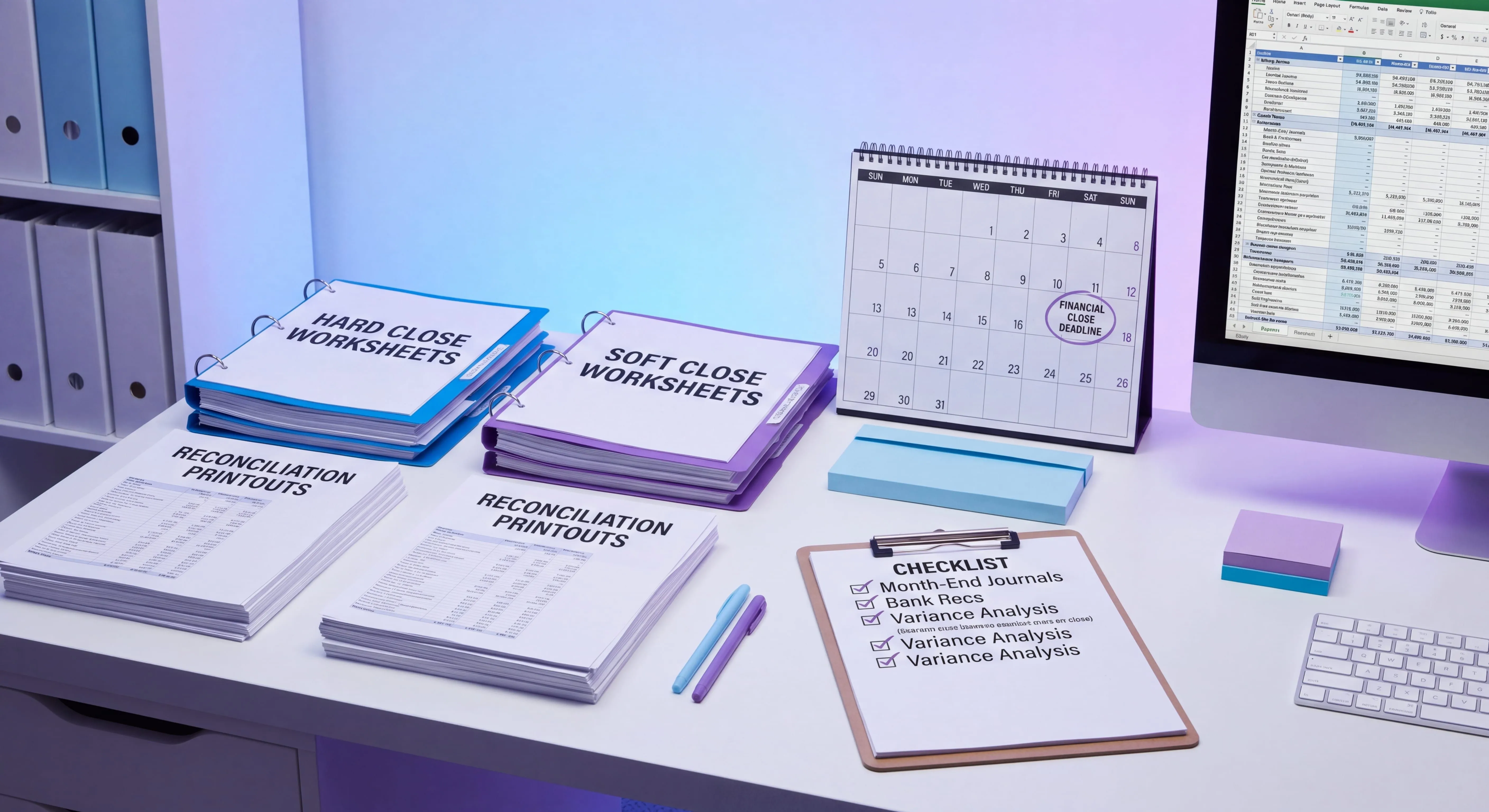

Hard Close vs Soft Close

This is the single most useful concept in the whole process, and it’s the one most teams have never explicitly defined.

Soft Close

A soft close is a fast, lightweight close. You book the big, obvious items, do the reconciliations that move the numbers materially, and produce management financials that are directionally accurate: good enough to make decisions, not good enough to file.

Soft closes show up monthly, and especially mid-quarter. The point is speed and visibility. You’re trading a little precision for getting numbers in front of leadership three or four days after month-end instead of ten.

What you typically skip or estimate in a soft close:

- Small accruals that won’t change the story

- Immaterial reconciling items left for the next period

- Deep subledger tie-outs where you trust the system

- Full supporting documentation for every entry

Hard Close

A hard close is the real thing. Every account is reconciled, every accrual is booked, every subledger ties to the general ledger, supporting documentation exists for each material entry, and once it’s done, the period is locked and nobody reopens it without a formal exception.

You run a hard close at quarter-end and year-end at minimum. Plenty of teams hard-close every month. That’s the gold standard, but it’s expensive in hours, which is exactly why the soft-versus-hard decision should be a documented policy, not a vibe.

Here’s the mistake I see constantly. A team thinks it does a hard close every month, but in practice it’s been doing soft closes and discovering surprises at year-end. Writing down which months are soft and which are hard removes that entire category of nasty surprise.

Teach your co-workers or customers how to get stuff done – in seconds.

The Financial Close Timeline

A close is a sequence with dependencies, not a month-end checklist you can run in any order. Roughly, it looks like this, measured in business days after period-end (BD+1 = first business day after the period closes). APQC benchmarking of more than 2,300 organizations puts the median close at 6.4 calendar days, with top-quartile performers finishing in 4.8 days or fewer. The bottom quartile takes 10 or more days - a gap that almost always traces back to undocumented steps, unclear ownership, and inconsistent reconciliation discipline rather than accounting complexity.

BD+1 to BD+2, cut off and capture. Stop the period. Make sure all transactions that belong to the period are in: vendor invoices, customer invoices, payroll, expense reports, corporate card activity. Anything still in transit gets accrued. A clean cutoff is the foundation. A sloppy one poisons everything downstream.

BD+2 to BD+4, reconcile. Cash first, then the high-risk balance sheet accounts. Bank reconciliation is the anchor. If cash doesn’t tie, nothing else can be trusted. Then AR, AP, prepaids, accruals, fixed assets, and intercompany.

BD+3 to BD+5, adjusting entries. Book accruals, deferrals, depreciation, amortization, and any reclasses. This overlaps with reconciliation on purpose; the rec work surfaces most of the entries you need.

BD+4 to BD+6, review and analyze. Run the trial balance, do a flux/variance analysis against prior period and budget, and chase down anything that doesn’t have an explanation. This is where a controller earns their salary. Not in booking entries, but in knowing which variances are real and which are errors.

BD+5 to BD+7, lock and report. Sign off, lock the period in the system, and produce the financial statements and management reporting package.

For a soft close, compress that into the first three or four days and accept the precision tradeoff. For a hard close, especially year-end, expect it to stretch, with audit support layered on top.

The exact day count matters less than the order and the ownership. Every step needs a named owner and a defined predecessor, or the close turns into a daily standup of “wait, is that done yet?”

The Controls That Keep a Close Honest

A close without controls isn’t a close. It’s a hopeful guess that happens monthly. These are the controls that actually matter:

- Segregation of duties. Whoever prepares a reconciliation or journal entry should not be the same person who approves it. This is the foundational control and the first thing an auditor checks. My internal controls in accounting post goes deep on this.

- Reconciliation sign-off. Every material account reconciliation gets reviewed and explicitly approved by someone other than the preparer, with the reconciling items explained, not just the balance agreed.

- Journal entry approval. Manual entries, especially top-side and adjusting entries, need documented approval and a clear business reason. Manual entries are where both honest mistakes and fraud live.

- Cutoff controls. Defined rules for what belongs in the period, so revenue and expenses land where they actually occurred.

- A locked period. Once closed, the period is locked. Reopening requires a documented exception and re-approval. An open period is an editable period, and editable history is no history at all.

- An audit trail. Who did what, when, and why, preserved. That’s what turns “trust me” into “here’s the evidence.” See how a proper audit trail works for why this is non-negotiable.

If you’re formalizing these, treat them as a system, not a list. That’s the argument I make in the financial controls guide.

How the Financial Close Differs From a Basic Month-End Close

People use the terms interchangeably, and mostly that’s fine. But there are real differences worth being precise about. Ventana Research found that 54% of organizations that use automated workflows to manage their close complete it within six business days, versus just 21% of those using little or no automation. That 33-point gap shows up most sharply between monthly and year-end closes, where the control intensity and documentation requirements are highest.

- Scope. A month-end close is one period. The financial close process spans monthly, quarterly, and annual closes, each with escalating rigor.

- Depth. Month-end is often a soft close in practice. Quarter-end and year-end are hard closes by necessity. Quarter-end may involve external reporting, year-end involves the auditors.

- Audience. Monthly numbers serve internal management. Quarterly and annual numbers serve the board, lenders, regulators, and auditors. The audience determines the required precision.

- Controls intensity. The control set is the same in name, but year-end runs it at full strength with external scrutiny on top.

The practical takeaway: don’t design a single generic close. Design a close backbone, then define soft and hard variants of it, and write down which periods get which.

Document It Once So It Survives the People Who Run It

Here’s the part nobody likes to admit. For most teams, the financial close doesn’t really live in the ERP or the checklist spreadsheet. It lives in the controller’s head. Which account to reconcile first. Which subledger always ties out late. Which manager you have to email twice. Which entry is “the weird one we book every December.”

That works right up until that person is on vacation during close week, or leaves. Then the close, the thing the entire company’s reporting depends on, walks out the door with them.

That’s exactly the problem I built Glitter AI to solve. Instead of writing a 40-page close manual nobody updates, you click through your actual close one time, the reconciliations, the entries, the reviews, in your real systems, and Glitter turns it into a clean, visual, step-by-step guide with screenshots, automatically. Next month, whoever runs the close follows the guide instead of channeling the controller’s memory. When the process changes, you re-record the step that changed instead of rewriting a document.

A documented close is the difference between a process and a single point of failure. It’s also, not coincidentally, what auditors love to see. For the broader pattern of standardizing finance work this way, the glossary entry on standardizing accounting procedures is good background.

Teach your co-workers or customers how to get stuff done – in seconds.

A Quick Playbook

If you want to tighten your close starting this period, do these four things in order:

- Write down whether each month is a soft or hard close. Just deciding this explicitly fixes more than you’d expect.

- Assign a named owner and a predecessor to every close task. No orphan steps, no “who’s doing the bank rec?”

- Make preparer ≠ approver real, not theoretical. If the same person does and checks the work, you don’t have a control.

- Record the close once as a visual guide so next month doesn’t depend on the same brain being available.

None of this requires new software you don’t already have. It just requires the close to exist somewhere other than one person’s memory.

Frequently Asked Questions

What is the financial close process?

The financial close process is the recurring set of steps a finance team uses to finalize the books for a period and produce reliable financial statements. It includes capturing all transactions, reconciling accounts, booking adjusting entries, reviewing results, locking the period, and reporting.

What is the difference between a hard close and a soft close?

A soft close is a fast, lightweight close that produces directionally accurate management numbers by booking only material items. A hard close reconciles every account, books every accrual, ties out all subledgers, and locks the period so it can't be changed without a formal exception.

How is the financial close different from the month-end close?

The month-end close is one instance of the financial close process. The financial close umbrella spans monthly, quarterly, and annual closes, with depth, audience, and control intensity increasing as the stakes rise - year-end being the heaviest because auditors are involved.

How long should the financial close take?

A soft close typically targets three to four business days after period-end. A hard close commonly runs five to seven business days, and year-end stretches longer once audit support is layered on. The order of steps and clear ownership matter more than the exact day count.

What are the main steps in the close timeline?

Cut off and capture all period transactions, reconcile cash and high-risk balance sheet accounts, book adjusting entries, review with a variance analysis, then lock the period and produce reporting. Reconciliation and adjusting entries overlap on purpose.

What controls are needed for a financial close?

Key controls include segregation of duties between preparer and approver, reconciliation sign-off, journal entry approval with a documented reason, cutoff controls, a locked period after close, and a preserved audit trail. Together these turn a hopeful estimate into a defensible close.

Why should the period be locked after closing?

An open period is an editable period, which means prior results can change silently and the audit trail loses meaning. Locking the period and requiring a documented exception to reopen it protects the integrity of reported numbers.

When should a company do a hard close versus a soft close?

Soft closes are common for interim months where speed and visibility matter most. Hard closes are required at quarter-end and year-end, and many strong teams hard-close every month. The decision should be a written policy, not an informal habit.

What is a flux or variance analysis in the close?

A flux or variance analysis compares current-period balances against prior period and budget to find unexpected movements. It's how a controller catches errors and confirms that real changes have real explanations before the books are locked.

How do you document a financial close process?

The most durable approach is to capture the close as a visual, step-by-step guide recorded from the real systems and steps, rather than a static manual nobody updates. Tools like Glitter AI generate this automatically by recording the process once, so the close survives turnover and vacations.