Read summarized version with

A finance lead at a 60-person company once told me her expense policy was “the PDF nobody reads until they want money back.”

She wasn’t wrong. The policy existed. It lived in a shared drive folder three clicks deep. It had everything in it - per diems, mileage rates, approval tiers - and almost nobody followed it, because almost nobody had read it. Every month the expense report process handed her a pile of claims with missing receipts, mystery dinners, and a $400 monitor someone bought without asking. Every month she’d play detective instead of doing her actual job. The underlying numbers make the case for doing better: a GBTA Foundation study found that roughly one in five expense reports contains errors or missing information, costing an additional $52 and 18 minutes to correct each flawed report - and the ACFE’s 2024 Report to the Nations found that expense reimbursement fraud appears in 13% of occupational fraud cases, with a median loss of $50,000 per incident.

That gap is the real problem with expense reimbursement. The policy is rarely wrong. The trouble is that it’s a document instead of a process people can actually run.

I’m Yuval, CEO of Glitter AI. We help finance and ops teams turn the procedures buried in their drives into step-by-step guides people follow without asking. This is what I’ve learned about writing an expense reimbursement policy that holds up - the components it needs, how to set limits and approval, and how to make the documentation requirements stick. There’s a free template at the bottom you can fill in today. Jump to downloads section.

Teach your co-workers or customers how to get stuff done – in seconds.

What an Expense Reimbursement Policy Actually Is

An expense reimbursement policy is the documented rules for which business expenses your company pays back, who approves them, how much is allowed, and what proof an employee has to provide. It’s the contract between “I spent my own money for work” and “the company pays me back.”

If you want the formal background on how a policy differs from the step-by-step procedure that enforces it, the glossary entry on policy vs. procedure covers that distinction well. Short version: the policy says what’s allowed, and the procedure says how a claim moves from submission to payment. You need both. Most teams only have the first.

A good policy answers four questions for every expense:

- Is this reimbursable? (eligible vs. non-reimbursable categories)

- How much is allowed? (spending limits and per diems)

- Who approves it? (approval authority by amount)

- What proof is required? (documentation requirements)

Get those four right and you’ve eliminated most of the back-and-forth that makes expense season miserable for finance and HR.

The Core Components of an Expense Reimbursement Policy

Every policy worth circulating has the same backbone. Skip a section and that’s where the disputes show up later.

1. Purpose and Scope

State why the policy exists and who it covers. Sounds like filler, but scope is where I see the most expensive ambiguity. Does it cover contractors? Part-timers? International employees on a different per diem? Officers with corporate cards? Spell it out so nobody gets to argue they weren’t covered.

2. Eligible Expenses

List the categories you actually reimburse, with the conditions attached. Be specific:

- Travel: airfare class caps, lodging per-night caps, ground transport, parking, tolls

- Meals: business meal limits or a per diem, tip caps, attendee rules

- Mileage: reimbursed at the current IRS standard rate for personal vehicle use

- Supplies and tools: the dollar threshold below which someone can buy without pre-approval

- Professional development: conferences, training, memberships, with prior approval

The rule that ties it together: an expense has to be for a legitimate business purpose, be reasonable, and be documented. Those three words - purpose, reasonable, documented - should appear early and get repeated.

3. Non-Reimbursable Expenses

This is the section people skip and later regret. Listing what you won’t pay for heads off the awkward one-off rejections that feel personal. Common ones: personal expenses, alcohol unless pre-approved, traffic and parking fines, late fees, personal subscriptions, and anything submitted past the deadline. Put them in writing and the answer becomes “the policy says no,” not “I decided no.”

4. Spending Limits and Per Diems

Limits are what make a policy enforceable instead of aspirational. Set a cap per category and a per diem for meals. The point isn’t to be stingy. It’s to take judgment calls off the table so a $90 airport dinner doesn’t turn into a 20-minute conversation.

5. Approval Authority

Tie the approver to the dollar amount. A tiered table works better than prose because it’s unambiguous at a glance:

| Expense amount | Approver | Documentation |

|---|---|---|

| Up to $250 | Direct manager | Itemized receipt + business purpose |

| $250 - $1,000 | Department head | Receipt + manager pre-approval |

| Over $1,000 | Finance Director | Receipt + written justification |

| Out of policy | Controller / CFO | Exception request + rationale |

The dollar figures are yours to set. The structure - escalating authority with escalating documentation - is the part that matters. This is really just an approval workflow applied to spend, and the same principles that make any approval workflow work apply here: clear thresholds, named approvers, no self-approval.

6. Documentation Requirements

Be precise about proof. “Submit a receipt” is not a requirement; it’s a hope. Specify:

- An itemized receipt (not the card slip) for anything over your threshold

- Date, vendor, amount, and business purpose per line

- Attendee names and affiliations for meals

- A project or cost-center code for allocation

- Manager pre-approval attached for travel and large expenses

7. Submission Process and Deadlines

A deadline with no consequence isn’t a deadline. State the submission window (e.g., 30 days from the expense date), the manager review SLA, and the reimbursement timeline. Then state what happens to late claims. Without that last part, every deadline is optional.

8. Compliance and Controls

This is the part auditors care about. The ACFE identifies lack of internal controls as the leading contributing factor in occupational fraud, cited in 32% of cases - and expense reimbursement is one of the schemes most affected by weak oversight. The one non-negotiable: the person who incurs an expense cannot approve their own reimbursement. Add spot audits, a records retention period, and the consequences for violations. If you already run finance controls, this should mirror them. My broader guide to documenting finance procedures covers how expense controls fit into the wider finance control environment, and a clean audit trail on every claim is what makes the whole thing defensible at year-end.

Teach your co-workers or customers how to get stuff done – in seconds.

Setting Limits That People Actually Follow

The mistake I see most often is setting limits in a vacuum. Someone picks “$75 for dinner” because it feels about right, never benchmarks it, then spends the next two years approving $90 exceptions.

A few things that actually work:

- Benchmark against reality. Pull last year’s actuals. If the median business dinner is $85, a $50 cap just guarantees exception requests. Set the limit a little above where most legitimate spend already lands.

- Use per diems for high-volume categories. Meals and incidentals are where itemization burns the most time. A per diem trades a bit of precision for a big drop in review effort. Most finance teams come out ahead.

- Differentiate by geography if it matters. A $200 lodging cap is generous in one city and impossible in another. One flat number for everywhere is where half your exceptions come from.

- Make the exception path explicit. People will hit edge cases. When the policy says how to request an exception and who grants it, those turn into 30-second decisions instead of disputes.

The goal isn’t the tightest possible limit. It’s the limit that produces the fewest judgment calls.

Why Most Expense Policies Fail (And How to Fix It)

Here’s the uncomfortable part: most expense policies fail for the same reason that finance lead’s PDF failed. The rules are fine. The format is the problem.

A policy document is a reference. People only open it when they’re already confused, or already in trouble. By then the mistake is made. What finance and HR actually need is for the policy to show up the moment someone is about to submit a claim, as “here’s exactly what to do,” not “here are 11 pages, good luck.”

That’s the shift: from a policy people are supposed to have read to a procedure people follow in the moment. The components above are the policy. The submission steps, the screenshots of your expense tool, the “attach an itemized receipt here” - that’s the procedure, and it’s the part that actually changes behavior. This is the same reason a strong step-by-step procedure for paying invoices outperforms an AP policy memo: the SOP tells someone what to click, in order, while they’re doing the work.

This is exactly what we built Glitter AI for. You walk through submitting an expense once, in whatever tool you already use, and it captures every step into a guide with screenshots that anyone can follow. The policy stops being the PDF nobody reads and becomes the steps people actually take. If you’re documenting finance procedures more broadly, the finance department SOP guide covers how expense reimbursement fits alongside AP, AR, and close.

Teach your co-workers or customers how to get stuff done – in seconds.

How to Roll Out the Policy

Writing it is the easy half. Adoption is where policies go to die. A rollout that works:

- Draft from the template. Don’t start from a blank page. Fill in the bracketed sections below.

- Pressure-test with one team. Have a high-volume team run their next month of expenses against the draft. The disputes that surface are the gaps you need to close.

- Pair the policy with a procedure. Publish the rules and the step-by-step “how to submit” together. One without the other won’t change behavior.

- Make it findable at the moment of need. Link the procedure inside your expense tool, not three folders deep in a drive.

- Set a review cadence. IRS rates change and limits drift out of date. Put a review date on it and own it.

Downloads

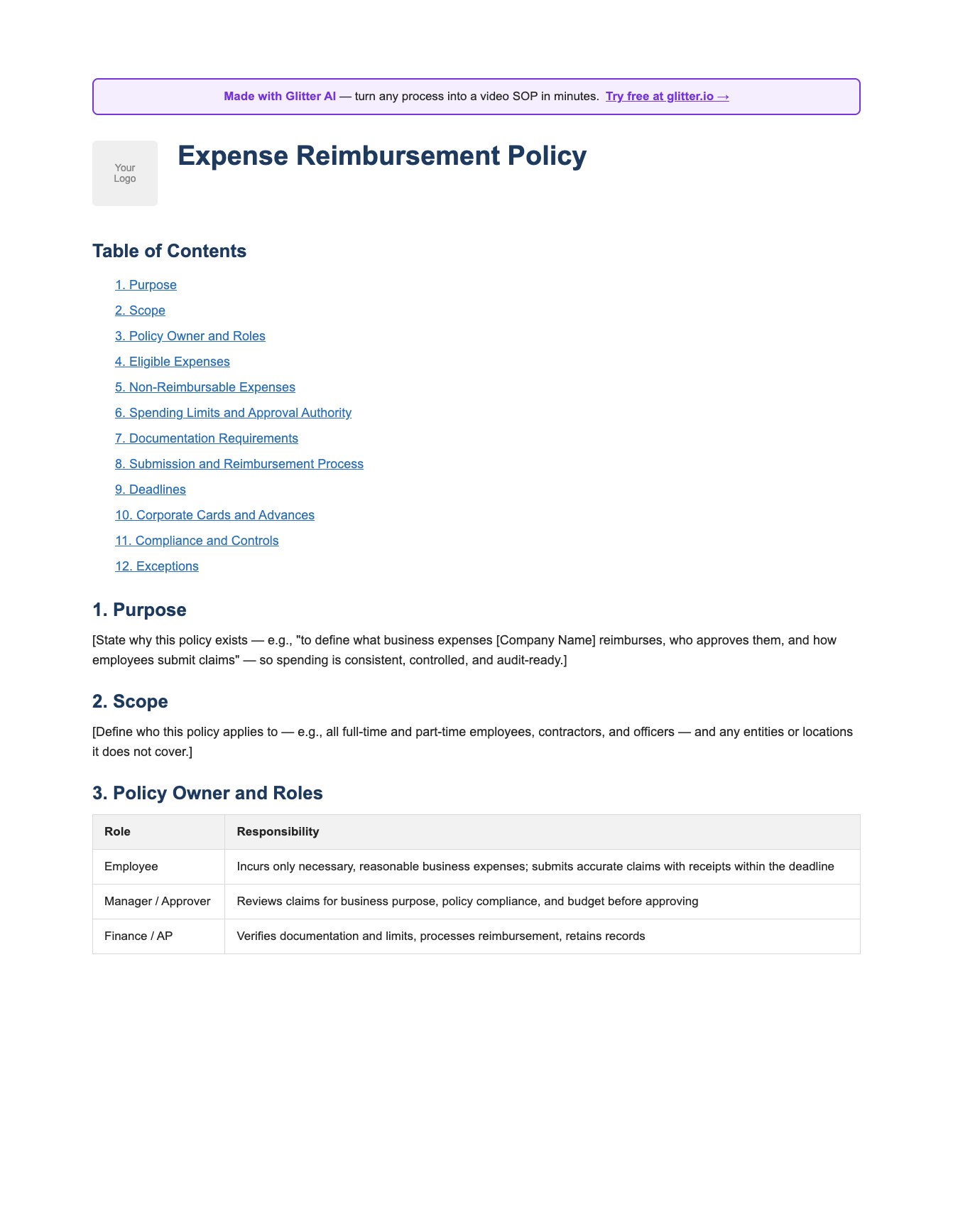

Download this free template, fill in the brackets, and circulate it for approval. It covers every component above: scope, eligible and non-reimbursable expenses, limits, tiered approval authority, documentation requirements, deadlines, and compliance controls.

Download the Expense Reimbursement Policy Template

A free Word template covering components, approval tiers, limits, and documentation. Fill it in and ship it today.

Download Expense Reimbursement Policy Template

Frequently Asked Questions

What is an expense reimbursement policy?

An expense reimbursement policy is the documented set of rules defining which business expenses a company pays back to employees, who approves them, the spending limits, and what documentation is required. It standardizes how claims are submitted, reviewed, and reimbursed so spending stays controlled and audit-ready.

What are the core components of an expense reimbursement policy?

The core components are purpose and scope, eligible expenses, non-reimbursable expenses, spending limits and per diems, approval authority, documentation requirements, submission deadlines, and compliance controls. Missing any one of these is usually where disputes and audit findings appear.

How should expense approval limits be set?

Tie the approver to the dollar amount using an escalating tier table, so larger expenses require higher authority and more documentation. Benchmark the dollar thresholds against last year's actual spend rather than guessing, and always require a second person to approve so no one approves their own reimbursement.

What documentation should an expense reimbursement policy require?

Require an itemized receipt (not just the card slip) for any expense above your threshold, plus the date, vendor, amount, and business purpose for each line. Meals should include attendee names, and every claim should carry a project or cost-center code for proper allocation.

What expenses are typically non-reimbursable?

Common non-reimbursable items include personal expenses, alcohol unless pre-approved, traffic and parking fines, late fees, personal subscriptions, and any claim submitted after the deadline. Listing these explicitly prevents one-off rejections from feeling arbitrary or personal.

What is a reasonable expense submission deadline?

Most companies require expenses to be submitted within 30 days of the date incurred, with manager approval and finance reimbursement following defined service levels. A deadline only works if the policy also states what happens to late claims, such as requiring policy owner approval.

Should we use per diems or itemized meal reimbursement?

Per diems work best for high-volume categories like meals and incidentals because they trade a small amount of precision for a large reduction in review effort. Itemized reimbursement gives tighter control but creates more work for both employees and finance, so most teams use per diems for meals and itemization for travel.

Who should own the expense reimbursement policy?

The policy is usually owned by the controller or a finance lead, who sets limits, handles exceptions, and schedules reviews. HR often co-owns communication and enforcement, since reimbursement intersects with payroll and employee relations.

How often should an expense reimbursement policy be reviewed?

Review the policy at least annually, and immediately when IRS mileage or per diem rates change. Put an explicit next-review date on the document and assign an owner so it does not drift out of date.

Why do expense reimbursement policies fail even when they're well written?

Most policies fail because they exist as a reference document people only open when already confused, not as a procedure they follow in the moment. Pairing the policy with a step-by-step submission guide that appears at the point of need is what actually changes behavior and reduces errors.