Read summarized version with

The first audit I ever sat near, I watched a controller spend three days doing nothing but answering the question “where is that document?”

The numbers were fine. The books were clean. But every PBC item turned into a treasure hunt: a bank statement in someone’s inbox, a lease buried in a shared drive, a depreciation schedule that only one person knew how to rebuild. The audit didn’t go long because the company was a mess. It went long because the company couldn’t find its own evidence quickly.

That’s the thing about audit prep, and the same is true of running your own internal audit checklist ahead of time. The work that actually slows you down usually isn’t accounting work at all. It’s retrieval work. And retrieval work happens to be exactly the kind of thing a checklist fixes. The stakes behind it are real: according to the ACFE’s 2024 Report to the Nations, the median time before a fraud case is detected is around 12 months, and lack of internal controls - the very thing auditors test - is the leading contributing factor in roughly 32% of fraud cases.

I’m Yuval, CEO of Glitter AI, and I spend a lot of time with finance teams who want audit season, like the rest of their bookkeeping checklist, to be predictable instead of a fire drill. So here is the full audit preparation checklist, organized by area, with a free downloadable version you can assign owners to and reuse every year. Jump to the downloads section if you just want the template.

Teach your co-workers or customers how to get stuff done – in seconds.

What an Audit Preparation Checklist Actually Does

An audit preparation checklist is the organized list of schedules, reconciliations, and source documents your finance team pulls together before the external auditors show up. It maps to the auditor’s PBC list (Prepared By Client), but it does a bit more than that. It assigns an owner to every item, tracks status, and records where each document lives so nothing turns into a treasure hunt during fieldwork.

A clean close and a clean audit are related but not the same thing. The financial close process produces accurate numbers. Audit prep proves those numbers to someone who wasn’t in the room. If you want the close side covered first, the month-end close checklist is the companion to this one.

Here’s the principle I’d tape to the wall: a good audit prep checklist makes your support findable, not just existent. A reconciliation isn’t done when it balances. It’s done when an auditor can open it, follow it, and tie it to the GL without asking you a single question.

The Full Audit Preparation Checklist by Area

Work these areas in roughly this order. Planning and the trial balance go first because everything else hangs off them. The document-heavy areas (cash, AR, AP) get a lot less painful once you’ve already pinned down where things live.

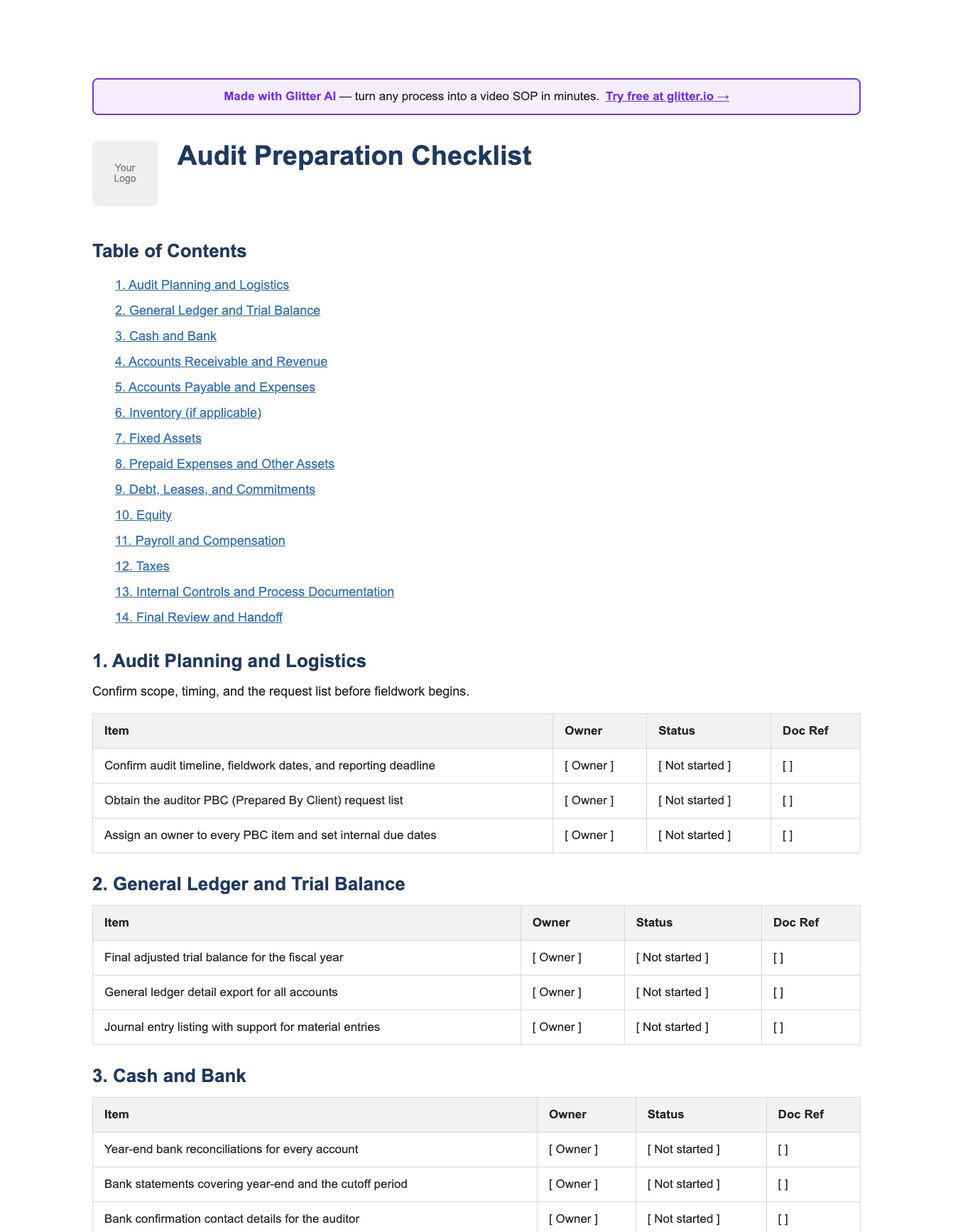

1. Audit Planning and Logistics

Before fieldwork, set the stage:

- Confirm the audit timeline, fieldwork dates, and the reporting deadline.

- Obtain the auditor’s PBC request list and read it line by line.

- Assign an owner to every PBC item with an internal due date earlier than fieldwork.

- Confirm every prior-year management letter point has been addressed.

- Set up one secure shared folder structured to match the PBC list.

Most “the audit ran long” stories trace right back to this section. A PBC list that lands two weeks before fieldwork and then just sits there unassigned is how a three-day audit turns into a three-week one.

2. General Ledger and Trial Balance

- Final adjusted trial balance for the fiscal year, locked.

- General ledger detail export for all accounts.

- Journal entry listing, with support attached for material and manual entries.

- Chart of accounts plus any mid-year mapping changes.

- Prior-year versus current-year variance analysis by account.

Auditors start here, so you should too. Every other schedule eventually has to tie back to this trial balance. A TB that’s still moving is a TB that isn’t ready.

3. Cash and Bank

- Year-end bank reconciliations for every account.

- Bank statements covering year-end and the cutoff period.

- Contact details so the auditor can send bank confirmations.

- A schedule of restricted cash and any compensating balances.

Cash is the easiest area to make airtight, and the worst one to fumble. If your year-end reconciliations are clean and documented the way I describe in the bank reconciliation process walkthrough, this section pretty much closes itself.

4. Accounts Receivable and Revenue

- Aged accounts receivable detail at year-end.

- Allowance for doubtful accounts calculation with support.

- Revenue recognition memo and a sample of key contracts.

- Sales cutoff support: the last invoices of the year and the first of the next.

- Deferred and unearned revenue rollforward.

Revenue is where auditors spend most of their time, so it’s where your support needs to be cleanest. Cutoff is the quiet trap here. A shipment recorded a day early can unravel an afternoon of testing.

Teach your co-workers or customers how to get stuff done – in seconds.

5. Accounts Payable and Expenses

- Aged accounts payable detail at year-end.

- Search for unrecorded liabilities: payments made after year-end with support.

- Accrued liabilities schedule with backup.

- Expense cutoff support around year-end.

- A listing of significant contracts and commitments.

The unrecorded liabilities search is the one teams underestimate, year after year. Auditors will pull post-year-end payments and ask which period they belong to. Build that support before they ask.

6. Inventory (if applicable)

- Year-end inventory listing valued at cost.

- Physical count instructions and completed count sheets.

- Inventory reserve and obsolescence calculation.

- Cost flow assumption memo and standard cost support.

If you carry inventory, the auditor often observes the physical count. Having the count instructions written down before count day is the difference between a smooth observation and an awkward one.

7. Fixed Assets

- Fixed asset register showing additions and disposals.

- Depreciation schedule reconciled to the GL.

- Support for major capital additions during the year.

- Impairment assessment, if applicable.

8. Prepaid Expenses and Other Assets

- Prepaid expense schedule with amortization support.

- Other asset rollforwards with documentation.

- Intangible asset and goodwill support, if applicable.

9. Debt, Leases, and Commitments

- Debt agreements, amortization schedules, and covenant calculations.

- Lease agreements and the lease accounting schedule.

- Interest expense and accrued interest support.

- A schedule of contingencies, guarantees, and commitments.

Covenant calculations are worth running before the auditor asks. If a covenant is tight, you want to know that and have the math ready, not discover it live in fieldwork.

10. Equity

- Equity rollforward with contributions and distributions.

- Cap table, stock and option agreements, and grant detail.

- Stock-based compensation expense calculation.

11. Payroll and Compensation

- Payroll register and year-end payroll reconciliation.

- Accrued wages, PTO, bonus, and commission support.

- Payroll tax filings and benefit plan documentation.

12. Taxes

- Income tax provision and supporting workpapers.

- Filed tax returns and any notices received.

- Sales, use, and payroll tax filings and reconciliations.

- Deferred tax asset and liability support.

13. Internal Controls and Process Documentation

- Process narratives or SOPs for key cycles: revenue, purchasing, payroll, and the close.

- Segregation of duties matrix and recent access reviews.

- Documented key controls and evidence they actually operated.

- A reconciliation log with preparer and reviewer sign-off.

- IT general controls and system change documentation.

This is where audit prep stops being about documents and starts being about how you actually run the place. Auditors don’t just want to see the control. They want to see it operated all year. A clean audit trail and a real set of internal controls in accounting turn walkthroughs from interrogations into confirmations.

14. Final Review and Handoff

- Tie every PBC item to its supporting document and its owner.

- Run an internal review of all schedules before the auditor sees them.

- Confirm the financial statements tie to the trial balance.

- Prepare the draft disclosure checklist and footnotes.

- Log open items and assign owners for fieldwork follow-up.

The internal review is the step that earns its keep. An auditor finding your error costs days. You finding it the week before costs about an hour.

How to Make This Checklist Stick

A checklist that lives in one controller’s head works fine, right up until that controller is on PTO during fieldwork. Here’s how to make yours survive a person being out, a new hire, or a change of audit firm.

Assign one owner per area. Not “finance.” A person. “Someone will pull the lease support” is how the lease support doesn’t get pulled.

Map it to the PBC list once, then reuse it. The first year you align your internal checklist to the auditor’s request list is painful. Every year after that, it’s just a copy.

Document the work the way it actually runs. This is the part most teams skip, and it’s also the part that costs the most. The reason audit prep turns into a fire drill every year is that the how lives in people’s heads: how the deferred revenue rollforward gets built, how the covenant math works, which folder the bank confirmations go in. That’s the gap I built Glitter AI to close. Rather than writing a procedure manual nobody updates, you record yourself preparing a schedule once and Glitter AI turns it into a step-by-step guide with screenshots. Next year, whoever owns that item follows the guide instead of reverse-engineering it from scratch. If you want the broader picture, my guide to documenting the whole finance function covers how this fits alongside your broader financial controls.

Teach your co-workers or customers how to get stuff done – in seconds.

Downloads

Here’s the full checklist as a free Word template. It already has every area above, with Owner, Status, and Doc Ref columns so you can assign items, track progress, and record exactly where each document lives:

Download the Audit Preparation Checklist

A free Word template covering all 14 audit prep areas, with Owner, Status, and Doc Ref columns and sign-off fields. Assign items, track progress, and reuse it every audit.

Download Audit Preparation Checklist

Frequently Asked Questions

What is an audit preparation checklist?

An audit preparation checklist is the organized list of schedules, reconciliations, and source documents a finance team assembles before external auditors arrive. It maps to the auditor's PBC list, assigns an owner to every item, and records where each document lives so fieldwork moves quickly.

What should be included in an audit preparation checklist?

A complete checklist covers audit planning and logistics, general ledger and trial balance, cash and bank, accounts receivable and revenue, accounts payable and expenses, inventory, fixed assets, prepaid expenses, debt and leases, equity, payroll, taxes, internal controls and process documentation, and a final review and handoff.

What is a PBC list in an audit?

PBC stands for Prepared By Client. It is the list of documents and schedules the auditor asks the company to prepare and provide before and during fieldwork. A good audit preparation checklist mirrors the PBC list and assigns an internal owner and due date to every item.

How do I prepare for a financial statement audit?

Start by obtaining the auditor's PBC list and assigning an owner and internal due date to each item. Lock the adjusted trial balance, complete and document all reconciliations, gather source documents into a structured shared folder, and run an internal review before handing anything to the auditor.

When should audit preparation start?

Audit preparation should start as soon as the year-end close is complete and the PBC list is received, ideally several weeks before fieldwork. Teams that wait until fieldwork begins to assign owners and gather documents are the ones whose audits run long.

What is the difference between the close and audit preparation?

The financial close produces accurate numbers by finalizing the books. Audit preparation proves those numbers to an independent auditor by assembling the support, reconciliations, and documentation needed to verify them. A clean close makes audit prep faster but does not replace it.

Why do audits run longer than expected?

Audits usually run long because of retrieval problems, not accounting problems: documents that are hard to find, schedules only one person knows how to build, and PBC items with no assigned owner. A checklist that tracks owner, status, and document location fixes most of this.

What documents do auditors typically request?

Auditors commonly request the adjusted trial balance and general ledger, year-end bank reconciliations and statements, aged AR and AP detail, revenue recognition support, fixed asset and depreciation schedules, debt and lease agreements, payroll and tax filings, and documentation of key internal controls.

How can process documentation speed up an audit?

When key processes like the revenue cycle, reconciliations, and the close are documented as step-by-step procedures, auditor walkthroughs become confirmations instead of interrogations, and any team member can prepare the supporting schedule the same way every year. This reduces back-and-forth and shortens fieldwork.

Is there a free audit preparation checklist template?

Yes. The free downloadable Word template in this post covers all 14 audit preparation areas with Owner, Status, and Doc Ref columns and sign-off fields, so finance teams can assign items, track progress, and reuse it for every annual audit.